Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

If you’ve ever tinkered with systems, you probably know that feeling when everything suddenly shifts and the old rules just stop working—like when water suddenly turns to steam once it hits the right temperature. Something similar happened in the world of money on August 15, 1971.

That night, President Nixon cut into the middle of Bonanza to tell everyone that the US would stop letting people trade dollars for gold, at least for a while. It might have sounded like just another policy tweak, but really, it was as if someone swapped out the basic code that made the whole money system run. For ages, money was something you could hold onto, like a battery storing up your hard work, but after that announcement, it turned into more of an IOU—a promise from the government that you could trade your dollars for, well, more promises down the line.

A lot of us think of inflation as some kind of mistake, like if the folks at the Federal Reserve just worked a little harder, prices would stop creeping up. But if you look back through history, you start to see that inflation isn’t really an accident—it’s built into the system to keep things moving and avoid getting stuck. The trouble is, this built-in feature comes with a tradeoff: it changed what money means for savers, turning cash from something you could count on to hold its value into something that slowly loses its strength, kind of like an ice cube melting on the counter.

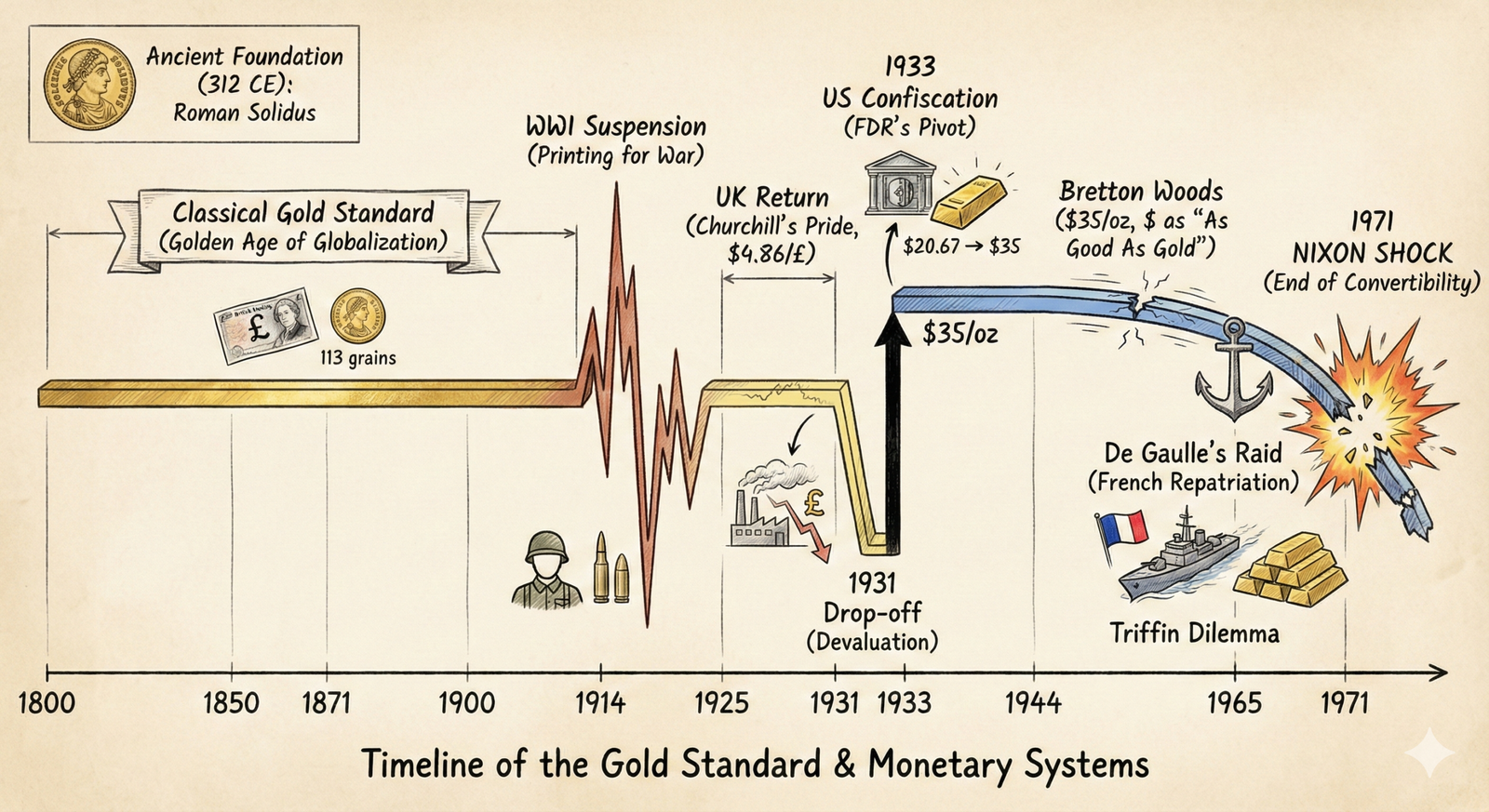

The Gold Standard Legacy

If we want to figure out why the system fell apart, it helps to look back at how things started. Gold wasn’t picked by a group of experts sitting around a table; it slowly became the standard because people all over the world kept choosing it, again and again, for thousands of years. Even though gold itself doesn’t change, the ways people tried to organize money around it turned out to be much more delicate than the metal they relied on.

If we trace the roots of stable money, we end up with the Roman Solidus, which was introduced way back in 312 CE by Emperor Constantine as a way to stop runaway inflation. This coin stuck around for about seven hundred years, earning a reputation as the Middle Ages’ version of the dollar. The big idea from this era was simple: money was just a certain weight of metal. During medieval times, Europe used both gold and silver, switching between them depending on what was coming out of the mines. The whole thing was a bit chaotic and no one was really in charge, but that messiness actually kept any one ruler from just making up new money whenever they wanted.

Moving into the 1800s, the world settled into what’s often called the Classical Gold Standard, which was really the high point of global trade and cooperation. Back then, money was just a name for a certain amount of gold—so, for example, a British Pound was simply 113 grains of pure gold. If one country bought more than it sold, gold would flow out to balance things out, so the system kind of kept itself in check. But there was a big problem hiding in plain sight: when countries suddenly needed to spend huge amounts of money, like during World War I, the gold standard just couldn’t keep up. The UK and others had to stop letting people trade their money for gold, because they needed to print more money to pay for the war, and gold was getting in the way.

After the war, Britain tried to get things back to how they were before, and in 1925, Winston Churchill brought the country back onto the Gold Standard at the old exchange rate of $4.86 per pound. The trouble was, the world had changed, and that price just didn’t fit the new reality. The result was falling prices and factories shutting down, which hit people hard. By 1931, with people rushing to take their money out of the banks, Britain gave up on gold again and let the pound drop in value to help its exports. This was a turning point, because it showed everyone that the promise to pay gold wasn’t set in stone after all.

While Europe was struggling, the United States took a very different approach. In 1933, during the depths of the Great Depression, President Roosevelt made it illegal for people to own gold, so everyone had to sell their gold to the government at $20.67 an ounce. Right after that, the government raised the price to $35 an ounce, which meant the dollar lost a lot of its value almost overnight. This move put most of the world’s gold into government hands and set things up for the next chapter in the story.

When World War II was over, the Allied countries met at Bretton Woods to figure out how to rebuild the world’s financial system. They came up with a new setup where the U.S. dollar was tied to gold at $35 an ounce, and all the other major currencies were tied to the dollar. For a while, having dollars was almost the same as having gold itself.

By the 1960s, though, the numbers just didn’t add up anymore. The United States was printing more and more dollars to pay for things like the Vietnam War and new social programs, until there were far more dollars out there than there was gold in the vaults. Seeing this, French President Charles de Gaulle decided to test the system by asking to swap France’s dollars for real gold, even sending ships to New York to pick it up. This rush for gold started to empty out U.S. reserves and made it clear that America couldn’t keep backing all those dollars with gold and still supply the world with money at the same time.

Why the Gold Standard Failed

The end of the Gold Standard wasn’t just about politics or bad intentions; it happened because the system ran into a problem it simply couldn’t solve, something people now call Liquidity Deadlock.

When you’re on a strict Gold Standard, the amount of money in the economy can’t go beyond the gold sitting in the vault, which might seem like a good idea until something goes wrong. Take the Panic of 1907, for example: it all started when the Knickerbocker Trust Company collapsed after a risky bet on copper went south, and as people hurried to pull out their money, the fear spread quickly. Since the U.S. money supply couldn’t stretch beyond the gold backing it, there was simply no way to create more cash to calm everyone down during the rush.

Everything ground to a halt, and it got so bad that J.P. Morgan had to gather the top bankers in New York into his own library, lock the doors, and keep the key in his pocket until they all agreed to put up their own money to save the trust companies. This bold move did stop the panic, but it left everyone uneasy, since it was clear that the whole system was depending on the personal fortune of just one man, which didn’t seem like a safe way to run a global economy.

The Great Depression showed another big problem, which economist Irving Fisher called the Debt-Deflation Spiral. In a gold-based system, when a credit bubble bursts and people start defaulting on loans, the total amount of money actually shrinks, which makes every dollar left more valuable. That might sound good, but if you’re someone who owes money, it’s a nightmare, because your debt gets harder to pay off just as your assets are losing value. Imagine owing $100, and then prices fall by 10%—suddenly, it’s like you owe $110 in real terms, even though your paycheck and the things you own are worth less. To try to pay back what you owe, you might have to sell off your stuff, which only pushes prices down further and makes the debt problem worse. This kind of downward spiral turned what could have been a regular recession into a full-blown depression, since central banks, stuck with the gold rules, couldn’t create the extra money needed to stop the cycle.

Structural Inflation & The Cantillon Effect

When we moved to using fiat money, which is really just money because the government says so, it gave us a way out of the old problem where there just wasn’t enough cash to go around in a crisis. Now, if something big happens—like what we saw in 2008 or 2020—the central bank can simply create as much money as needed to keep things from spiraling into a deflationary mess.

Of course, just like in engineering, fixing one problem usually means creating another, so while we solved the liquidity crunch, we ended up with something called structural inflation. When governments keep adding more money to the system to handle emergencies or cover their bills, each dollar (or whatever currency you use) slowly loses some of its buying power over time. But this inflation doesn’t hit everyone the same way, because of something called the Cantillon Effect, which is an old idea from the 1700s that still shapes how inequality works today.

Richard Cantillon noticed something interesting about how new money shows up in the economy, which is that it doesn’t just magically appear in everyone’s wallet at the same time; instead, it starts its journey at a few specific places, like when the government issues bonds or when banks make new loans, and from there, it slowly works its way through the rest of the system. So, if we follow the path of this new money, the first people to get their hands on it are usually the government and the big banks, which means they get to spend it while prices are still the same as before. Next, as the money keeps moving, it tends to flow into things like stocks and bonds, which pushes up the prices of those assets and makes the people who already own them even wealthier. Finally, after quite a bit of time has passed, the new money eventually reaches regular workers in the form of higher wages, but by that point, the cost of things like rent and groceries has already gone up, so it doesn’t feel like much of a win.

On top of all this, there’s something called financial repression, which just means that governments keep interest rates lower than inflation so they can slowly chip away at the huge debts they’ve built up. The catch is that this quietly eats into the savings of regular people, acting like a hidden tax that helps pay off public debt without anyone ever having to vote on it.

The Investment Mandate

So here’s the big idea that really changes how we think about investing today: it’s not so much about chasing riches as it is about making sure you don’t quietly lose what you already have. Back when money was tied to gold, there was this odd pattern called Gibson’s Paradox, where interest rates tended to rise along with prices. But once we moved to a world where money isn’t backed by anything physical, that old pattern flipped around. Now, things like gold and other solid assets tend to move in the opposite direction of real interest rates, which just means that when the returns on safe bonds can’t keep up with inflation, people start looking for safer ground by moving their money out of cash and into things that hold their value better.

This shift really turned the old rules about building wealth upside down. When money was getting more valuable over time, just holding onto cash made sense, since your savings would quietly grow all by themselves. But now, with inflation eating away at what your money can buy, cash starts to feel like something you want to pass along as quickly as possible, almost like playing a game of hot potato. Suddenly, just saving isn’t enough, and everyone is pushed into making choices about where to put their money, even if they’d rather just sit on the sidelines.

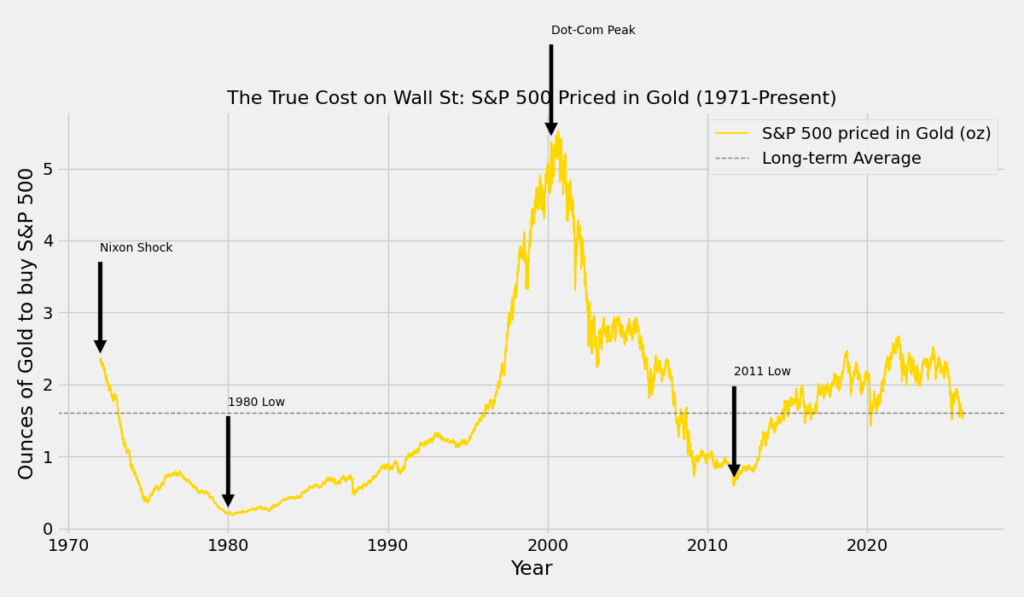

When we look at the stock market using dollars, it seems like it’s been shooting straight up for years, with the S&P 500 giving about 10% returns each year. But if we remember that the dollar itself keeps losing a bit of its strength over time, it’s like measuring your height with a ruler that keeps shrinking. To really understand what’s happening, it helps to look at stocks in terms of something that’s held its value for centuries, like gold. If you check out the chart below, you’ll see what the S&P 500 looks like when you measure it in ounces of gold instead of dollars, which helps cut through the fog that paper money can create.

If we look at the market through the lens of gold instead of dollars, the idea that stocks always go up starts to fall apart, and the first thing that jumps out is what happened during the 1970s. Even though the S&P 500 seemed to hold steady or even rise a bit if you just look at the dollar numbers, the reality was very different once you adjust for inflation, because in terms of gold, the value of the index actually fell off a cliff. The ratio of the S&P 500 to gold dropped from more than 2.5 ounces to less than 0.2 ounces, which means that people lost over 90% of their real wealth during that stretch.

Another thing that stands out when you measure everything in gold is just how wild the swings can be, because the biggest drop from peak to bottom in gold terms was over 92%, which is much steeper than the 56% drop you see if you only look at the dollar numbers. It really shows how using dollars as your measuring stick can hide just how rough the ride has actually been.

So if we fast forward to today, the S&P 500 is trading at about 1.58 ounces of gold, which is almost exactly the same as the average since 1971, sitting at 1.60 ounces. Even with all the excitement around AI and the fact that stock prices keep hitting new highs in dollar terms, what we really see is that stocks are just about fairly priced when you look at them in real terms. It’s not that we’re in some kind of bubble; it’s more that the dollars we use to measure everything have lost a lot of their punch.

Conclusion

When the world moved away from gold in 1971, it was a bit like switching from a machine with fixed parts to a program you can update as you go, which means the new system can handle surprises that would have broken the old one; but while it solved the problem of prices falling, it did this by making rising prices a built-in feature. So, if you’re someone trying to save money, it’s important to realize that holding onto cash is a bit like swimming against the current, since the system is designed to slowly eat away at the value of your savings. The way to keep the value of your work is to turn your cash into things that can keep up with all the new money being created, like stocks, real estate, or other assets that tend to rise over time, because in this new world, investing isn’t just for experts—it’s something everyone has to think about.

References

[1] “History of the Gold Standard,” World Gold Council.

[2] “Money and Banking in Medieval and Early Modern Europe,” Yale University.

[3] “The Classical Gold Standard,” National Bureau of Economic Research (NBER).

[4] “The Bretton Woods System,” Federal Reserve History.

[5] “The Panic of 1907,” Federal Reserve History.

[6] “The Great Depression and the Gold Standard,” history.com.

Leave a Reply