Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

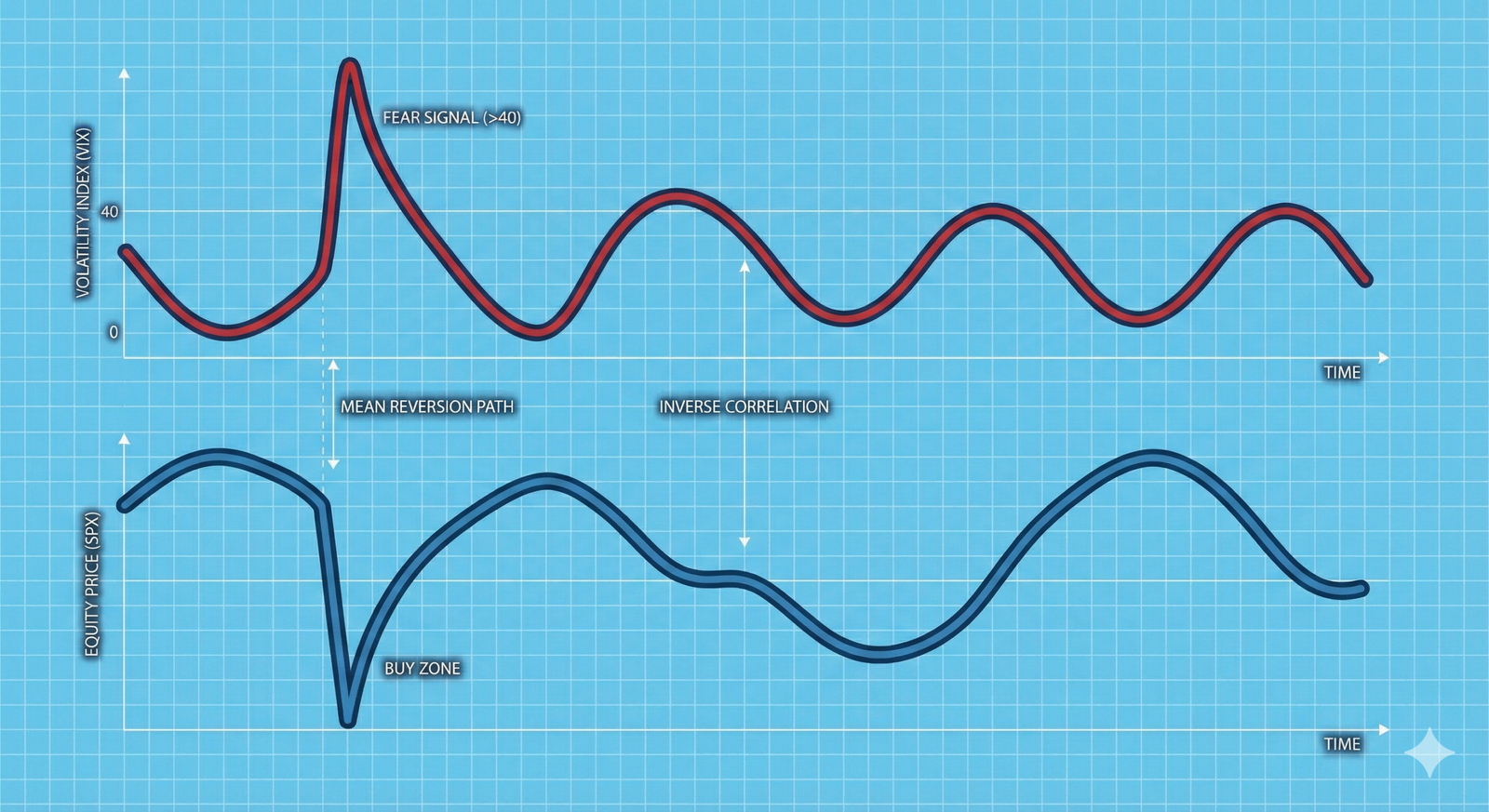

A lot of people look at volatility and see it as a kind of risk score, almost like a warning about how much money could disappear overnight, but I think that misses what volatility is really telling us. Instead of thinking about it as a measure of risk, I find it more helpful to see volatility as the price you pay for insurance. If you imagine the market as an insurance marketplace, there are times when the cost of protection gets so high that it stops making sense to buy it, and that’s often when it can actually make more sense to be the one offering that protection, especially when everyone else is rushing to get out.

If we borrow a bit of language from engineering, you can think of the VIX (which is just the market’s best guess at future volatility) as a kind of control signal that tends to snap back to its usual range over time. Unlike stock prices, which can wander off in any direction, volatility has some built-in limits: it can’t drop all the way to zero, since that would mean options are basically free, and it can’t stay extremely high for long, because the whole system would start to break down. These natural boundaries mean that volatility tends to swing back and forth in a way that’s actually pretty predictable, which gives us something to work with.

When I dug into the data for the S&P 500 and the VIX going all the way back to 1990, I wanted to see if this idea actually holds up. What I found is that if you treat fear not as something emotional, but as just another input you can measure and respond to, you end up with one of the few real advantages that still exist in a market where most other edges have disappeared.

The mirror effect

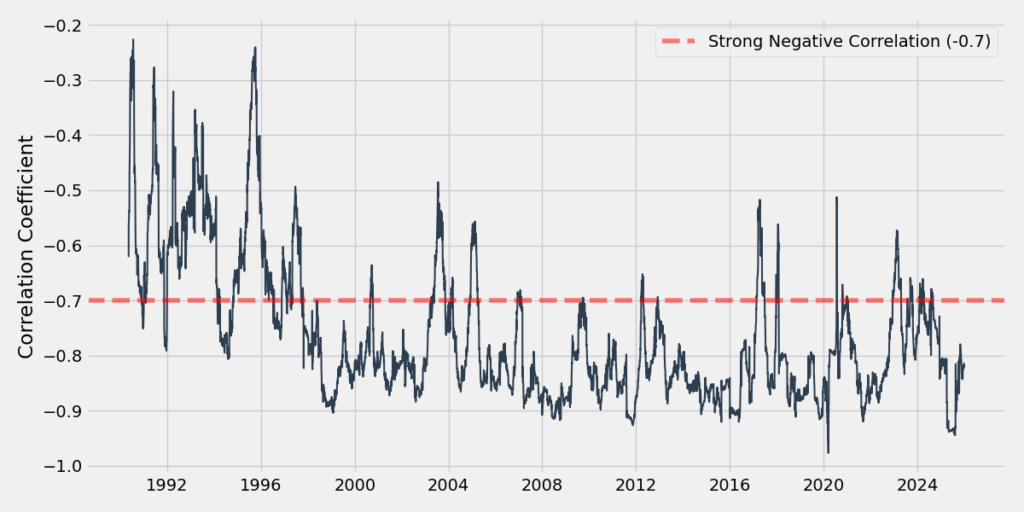

If you’ve ever watched the S&P 500 and the VIX move, you’ll notice they usually go in opposite directions, but it’s not a simple one-to-one relationship. The VIX, which is basically a measure of how much people expect the market to bounce around, comes from the prices of certain options on the S&P 500. Most of the time, things are pretty calm and the demand for these options is steady, but when the market takes a dive, everyone suddenly wants protection, so the demand for put options shoots up as big investors scramble to shield their portfolios. This rush pushes up the price of those options, which makes the VIX jump just as the S&P 500 is falling. To get a better sense of how this plays out over time, I looked at the 90-day rolling correlation between daily changes in the VIX and daily returns of the S&P 500.

If you look at the chart, you can spot a big change in how the market behaves. When things are calm and everyone feels good, the connection between price and volatility kind of drifts around, and sometimes it even disappears as people pile into call options hoping for more gains. But when the market gets rocky, which is exactly when these relationships really matter, the link between price and volatility snaps into place and gets much stronger. You can actually see this in the numbers, since the correlation drops well below -0.8 during tough times like the 2008 crisis and the 2020 crash.

You can think of this like a safety feature in engineering: when the market system starts to break down, the VIX steps in as a dependable mirror image of price. This shows us that volatility isn’t just random chaos; it’s actually the market’s way of reacting to how expensive it is to borrow money. So, when the correlation drops to -0.8, it’s almost as if the market is promising that falling prices will always come with rising fear. The interesting part, though, is that this fear doesn’t go on forever—it actually has a limit.

Buying the crash

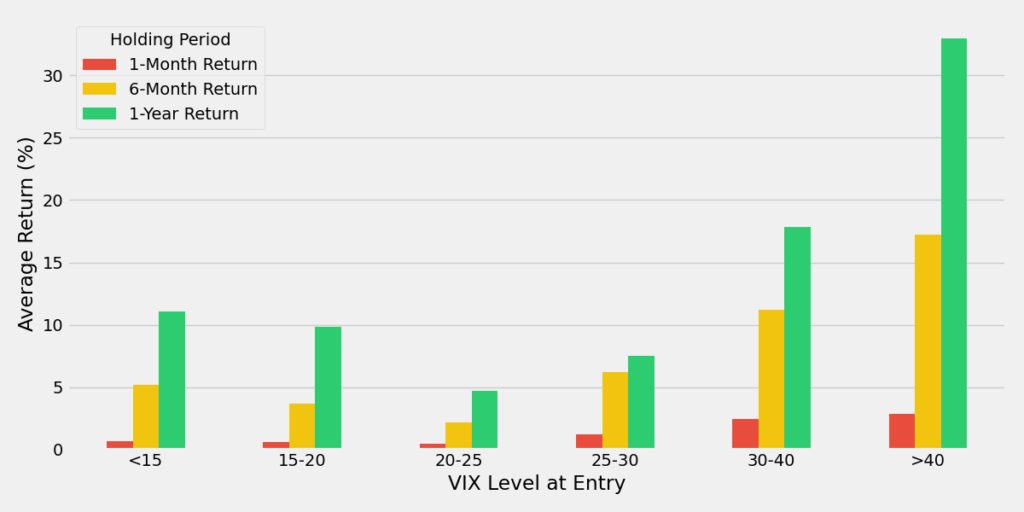

We’ve all heard the saying about buying when there’s blood in the streets, but the tricky part is figuring out what actually counts as ‘blood’—is it a five percent dip, a ten percent correction, or something else entirely? Since it’s so easy to get caught up in the mood of the market without any real guide, I like to use the VIX as a sort of panic thermometer, because it gives us a way to put numbers to those feelings. So, I went back and grouped different VIX levels from the past, then looked at how the S&P 500 performed over the next 1, 6, and 12 months, which helps us shift from just reacting to fear to actually measuring what kind of premium that fear might offer.

What we find here is surprising, and it goes against what you might expect at first glance. When the VIX is low, which I like to think of as the market’s comfort zone, it feels like a safe time to invest, but interestingly, that sense of safety comes at a cost, since buying during these calm periods has historically given you an average 12-month return of about 11 percent, which is really just the market’s usual pace when nothing exciting is happening.

When the VIX moves up into the low twenties, things get tricky, because this is often the point where the market is just starting to wobble, not finishing its drop, so if you buy here, the average 12-month return falls to only about 4.7 percent, which is much lower than the usual; this happens because professional investors are already getting cautious while most everyday investors haven’t reacted yet, so it’s a bit like stepping in just as things are getting unstable, rather than after the dust has settled.

But when the VIX shoots above 40, which only happens when fear in the market is really intense, buying at that point has historically led to an average 12-month return of 33 percent, which is a huge jump compared to the other scenarios.

So if you wait until the VIX reaches those extreme levels, your expected return over the next year is about three times higher than if you had bought during a quiet period, which really shows how the market rewards people who are willing to step in and buy when everyone else is too nervous to do so; it’s almost like the market pays you extra for being brave when things look the scariest, since, looking back, those moments have usually turned out to be the best opportunities.

Event studies

If you want to see how this actually plays out in the real world, it helps to think back to the two biggest shake-ups in recent memory: the 2008 Financial Crisis and the 2020 COVID Crash. Even though the reasons behind each were completely different—one was a meltdown in the banking system, while the other came out of nowhere as a global health crisis—the way the markets reacted, especially in terms of wild price swings, ended up looking almost exactly the same.

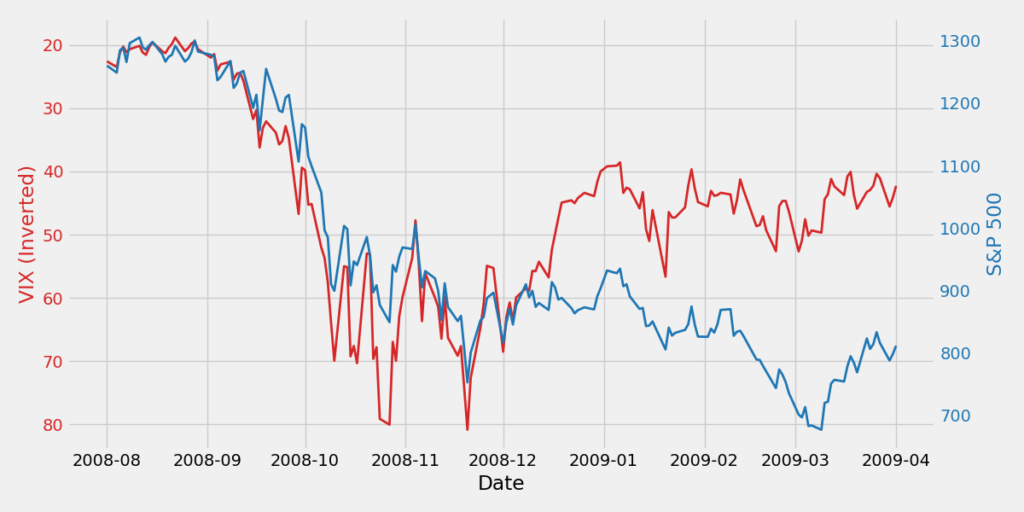

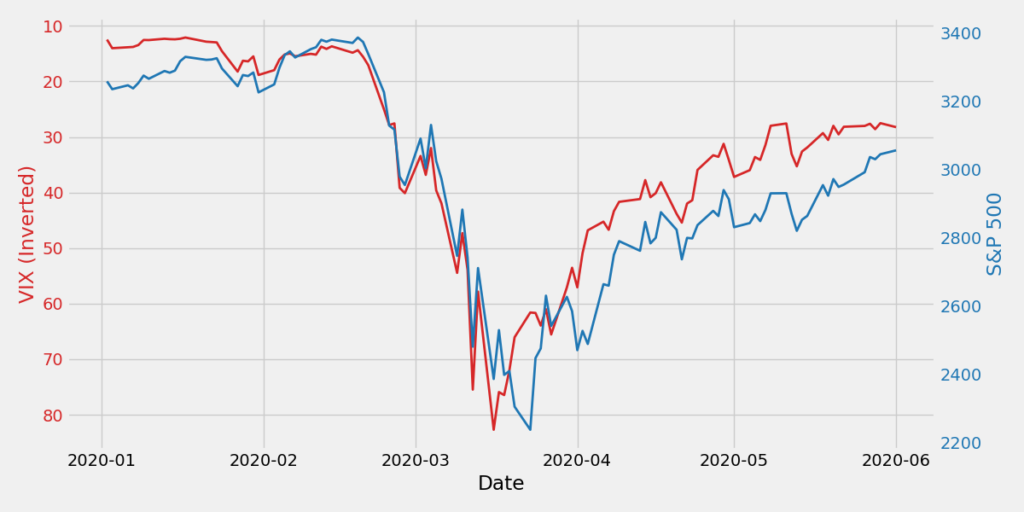

If you look back at 2008, you can see that the crash didn’t happen all at once; instead, it felt more like a slow leak that just kept getting worse as time went on. The VIX, which is that red line on the chart (and here it’s shown upside down), stayed high for months while big names like Lehman Brothers were falling apart, and it kept climbing as the situation got more tense. What’s interesting is that the very moment when the VIX hit its highest point in late 2008 was also when the market finally found its bottom, so even though stocks didn’t bounce back right away, the worst of the selling was over as soon as fear reached its peak.

If you think back to the 2020 crash, it really felt like the market was having a heart attack, since the S&P 500 dropped by 35% in just a few weeks, and at the same time, the VIX spiked to over 80 in mid-March, which actually turned out to be the exact week when the S&P 500 hit its lowest point.

What I noticed in both cases is that the first real sign of recovery didn’t come from the headlines or any official good news, but from the way volatility started to settle down before the fundamentals caught up, since prices only really found their footing after all that extra fear had worked its way out of the market; if you had waited for the reassuring news stories, you would have ended up buying back in at a much higher price, because the real clue was quietly sitting there in the option chain, not flashing across your news feed.

The asymmetry of fear

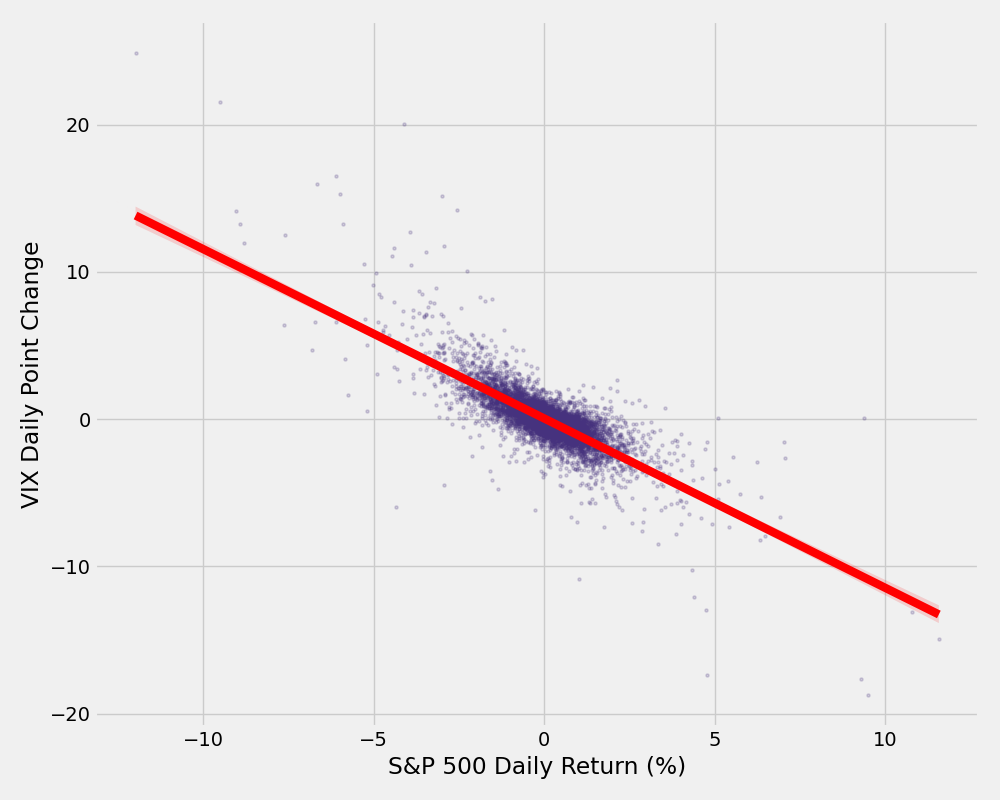

So, why does the VIX seem to jump so dramatically when the market gets shaky? It really comes down to something traders call the ‘asymmetry of fear,’ which is just a fancy way of saying that people react much more strongly to bad news than to good news. If you think about how stocks usually move, they tend to climb higher in slow, steady steps, but when they fall, it often feels like they’re dropping straight down. Volatility, which is what the VIX measures, picks up on this pattern. When I looked at daily returns, I saw this same effect: if you plot each day’s S&P 500 return against how much the VIX moved, you’ll notice that the relationship isn’t balanced. The line that best fits the data (which you can see in black on the chart) shows how much volatility tends to move for a given change in price.

If you look at the slope of that line, you’ll see it’s much steeper when the market falls than when it rises, which means that a big down day in stocks can send the VIX soaring, while a big up day only nudges it down a little. For example, if the S&P 500 jumps 2%, the VIX might drop by a point or two, but if the market falls by 2%, the VIX can easily shoot up by five points or more. This lopsided reaction is what makes volatility such a useful safety net: it tends to kick in right when you need it most, helping to cushion the blow when stocks are taking a hit.

The probability edge

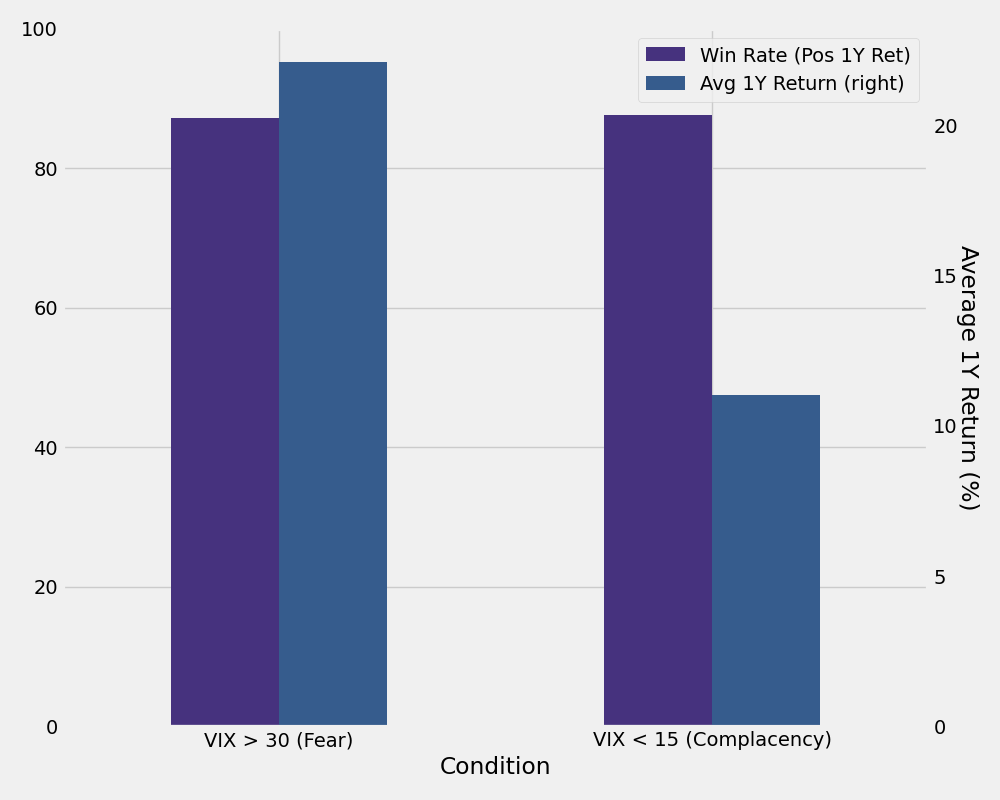

Let’s talk about that gut-level fear we all get when it feels like the market is in free fall, and the idea of buying when the VIX is up at 35 seems almost reckless, as if you’re just asking to get burned. It’s easy to believe that because things are crashing now, they’ll just keep crashing, but that’s really just our brains playing tricks on us—what’s called recency bias, where we expect the recent chaos to keep repeating. When I looked at the actual numbers, I found something surprising: if you buy when everyone is calm and the VIX is below 15, you have about an 88% chance of making money over the next year, but if you buy when fear is everywhere and the VIX is above 30, your odds are almost exactly the same. So, even though it feels scary, the data says that buying in those fearful moments is just as likely to work out as buying when things are quiet.

When you look at the numbers, the odds of winning or losing are pretty much the same whether the market feels calm or chaotic, so even though it might feel safer to buy when things are quiet, the reality is that your actual risk of losing money over a year is about 12% either way. The real difference comes down to what you stand to gain: in a low-volatility market, you are putting that 12% risk on the table for the chance at an 11% return, while in a high-volatility market, you are taking the same risk but the potential reward jumps to over 22%. If you think about it like tuning a radio, the best signal often comes through when there is a lot of static, because the payoff for tuning in is so much higher. In other words, you are getting twice the expected reward for the same risk, which is about as close as you get to having a real edge in the market.

Conclusion

I like to think of volatility as a kind of message from the market, not something to be afraid of, but more like a signal that tells you when money is hard to come by and when it is flowing more freely. The VIX, for example, is just a way of measuring how much people are willing to pay for protection, and when that price shoots up—say, four times higher than usual—it is a bit like everyone suddenly rushing to buy umbrellas because they think a storm is coming. In those moments, it often makes more sense to be the one selling the umbrellas rather than joining the crowd. You do not have to guess the headlines or try to outsmart the Fed; you just have to pay attention to what the market is telling you.

References

[1] CBOE VIX Whitepaper. Chicago Board Options Exchange.

[2] “Volatility as an Asset Class,” specific data derived from Yahoo Finance historical sets (^VIX, ^GSPC).

[3] Traub, B. “The VIX as a Market Timer.” Investopedia.

Leave a Reply