Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

Right now, it feels like the U.S. economy is trying to balance on a very thin wire, with a lot of debt on one side, some risky private lending on the other, and unpredictable energy prices shaking things up from below. For years, we kept the good times rolling by borrowing from the future—spending more than we had and keeping interest rates low to make it all seem manageable—but the numbers are finally starting to catch up with us as we head into 2026. While the financial system hasn’t fallen apart, you can sense that the pressure is building underneath, and it looks like we’re running out of room to keep spending more than we bring in, especially since our emergency reserves are basically empty.

All of this puts us in a spot where we might have to face a sudden, messy unwinding of debt, or maybe even a big reset in how money works in the U.S. If the Federal Reserve can’t pull off a very tricky balancing act, the Treasury could end up reaching for some unusual tricks, like changing how much the country’s gold is officially worth just to make the numbers work. People who are still using old playbooks from the 2010s are kind of flying blind right now, because the usual relationships between stocks, bonds, and the dollar aren’t holding up under the weight of a national debt that’s now almost $39 trillion.

If you think about it like an engineering problem, every system has a point where it just can’t take any more stress, and when that happens, things don’t usually break gently—they snap all at once. Right now, the global financial system is showing some of those classic warning signs that it’s being pushed past what it was built to handle. We’re seeing delays in how policy changes actually affect the economy, more friction when people try to borrow or lend money, and a growing pile of complicated financial promises on the government’s books. What’s interesting is that the next big problem probably won’t start with regular banks, but with these shadowy, tightly packed pools of private money that most people don’t see.

To really get what’s happening right now, I think we have to set aside the usual stories people tell about the economy and just look at how the system actually works, piece by piece. That means digging into what’s going on with shadow banking, checking how fragile our energy supply chain might be, figuring out the tough spot the Federal Reserve is in with the numbers, looking at how fast our national debt is growing, and seeing what options the Treasury has left if things get tight.

The $1.7 to $2.0 trillion private credit blind spot

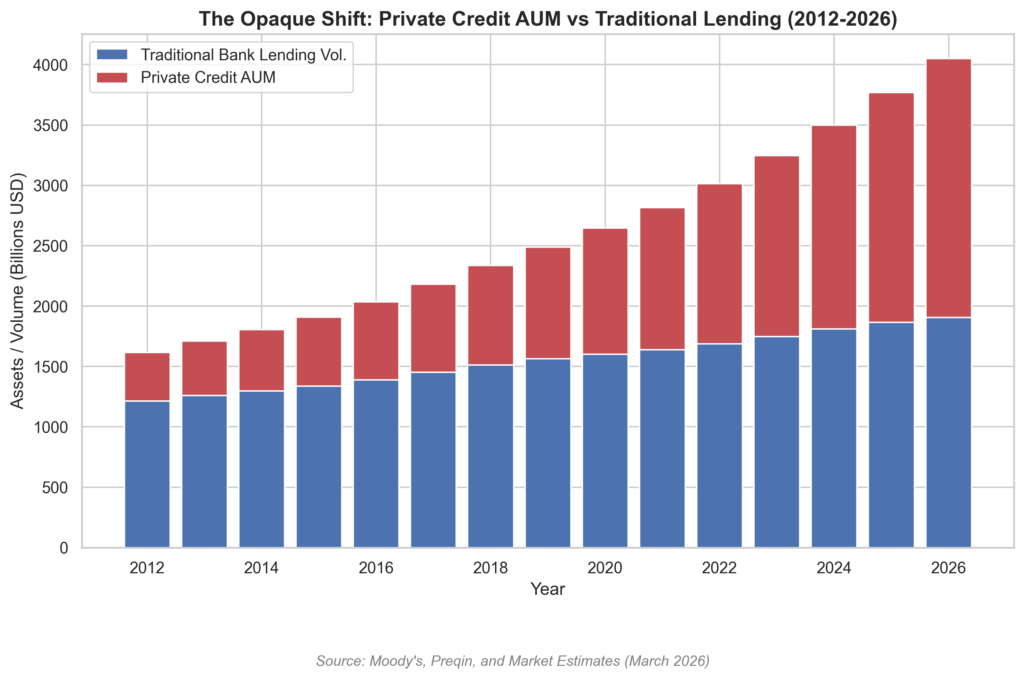

If you look at what’s happened over the past decade, you’ll see that private credit markets—those parts of the financial world that aren’t really watched or regulated like traditional banks—have grown at a pace that’s honestly hard to overstate. When new rules in the 2010s made banks pull back from taking big risks, it left a huge gap, and private equity firms and alternative asset managers were quick to fill it by lending money to companies that were already carrying a lot of debt, all in exchange for higher returns. The catch is that the loans behind these investments are pretty hard to sell in a hurry, so if investors suddenly want their money back all at once, the funds are stuck: they either have to sell what they own for much less than it’s worth, or just stop letting people take their money out altogether.

By March 2026, private credit had grown so much that it crossed the $2 trillion line, putting it right up there with the big players like leveraged loans and high-yield bonds. Both everyday investors and big institutions were drawn in by the promise of higher returns, even though the basic problem—where you can’t actually get your money out quickly if you need to—has been tripping up financial systems for as long as anyone can remember. It’s a bit like a hotel where your money can check in any time it wants, but if there’s a panic, it just can’t check out.

When I run this simulation, what really stands out is how quickly private credit has grown compared to traditional bank lending over the past fourteen years, and as the gap between the two keeps widening, it starts to look like a huge amount of money is quietly moving into these private funds that are hard to see into and not watched as closely, which means we have almost no idea how much pressure they might actually be under.

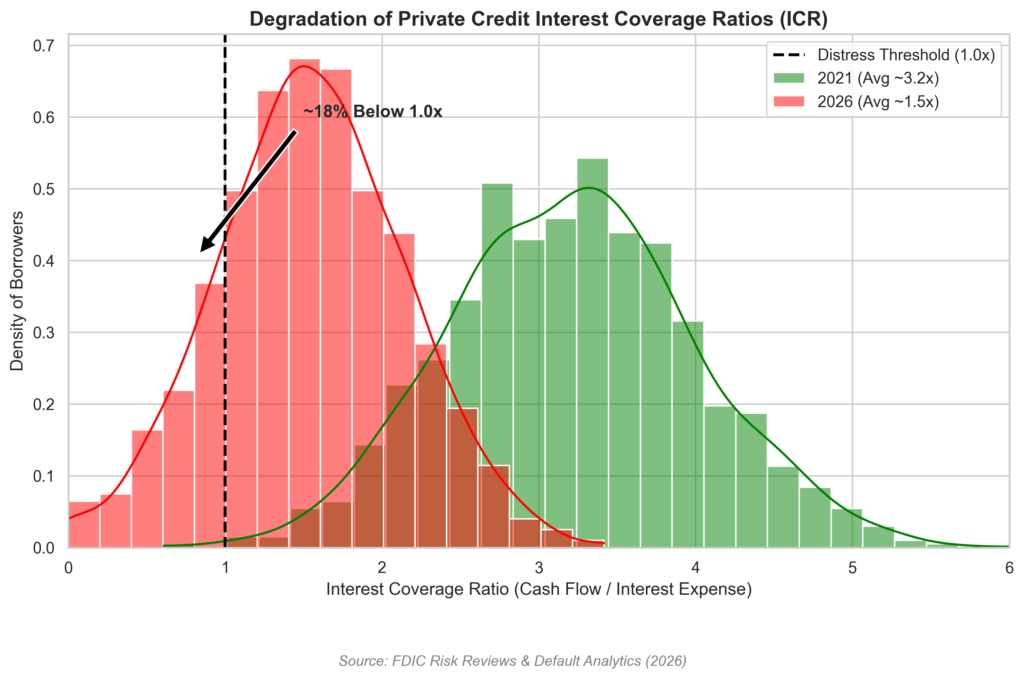

When you have this much capital sloshing around, lenders end up having to relax their standards, simply because there just aren’t enough top-tier borrowers to go around, and if you try to push two trillion dollars into a limited pool, some of it is bound to end up with companies that are a bit shaky. We’re already seeing the signs in the numbers: the FDIC recently pointed out that about 27% of private credit borrowers now have an interest coverage ratio below one, which is just a technical way of saying their regular business income isn’t enough to pay the interest on their loans.

If a company’s interest coverage ratio falls below one, it basically means they’re dipping into their savings or scrambling for new loans just to keep up with the interest on what they already owe, and that’s a tough spot to be in, especially now that borrowing is expensive and interest rates aren’t coming down anytime soon, so these companies are really feeling the squeeze.

It’s hard not to notice how much these coverage ratios have slipped, and if you line up the numbers from 2021 next to the early 2026 data, the shift toward financial trouble really jumps out, since the bulk of companies have moved much closer to that danger zone.

When enough borrowers start to struggle, things can quickly spiral, because the more people who fall behind, the faster the whole system starts to unravel. Many private credit funds use something called ‘payment-in-kind’ interest, which is really just a way for borrowers to roll their interest payments into the main loan instead of paying cash right now. This might buy everyone some time, but it also means the debt keeps growing in the background, so when it finally comes due, the amount owed can be much bigger than anyone expected. If things go wrong, the chances of getting much money back on these loans are pretty slim. And since the shadow banking world doesn’t have the safety net of the Federal Reserve to step in and calm things down, any panic here can pick up speed fast, because there’s no one to stop the slide until real damage is done.

Oil constraints and the depleted strategic petroleum reserve

If you think about it, energy really sits at the heart of everything we do in the economy, because when the price of oil suddenly jumps, it tends to ripple through every part of our lives, making things more expensive and sometimes even tipping us into a recession as people pull back on spending and companies struggle to keep up. Right now, the U.S. is in a particularly fragile spot, since ongoing conflicts around the world are putting a lot of pressure on the supply chains we all depend on, especially in those narrow stretches of ocean where so much oil has to pass through.

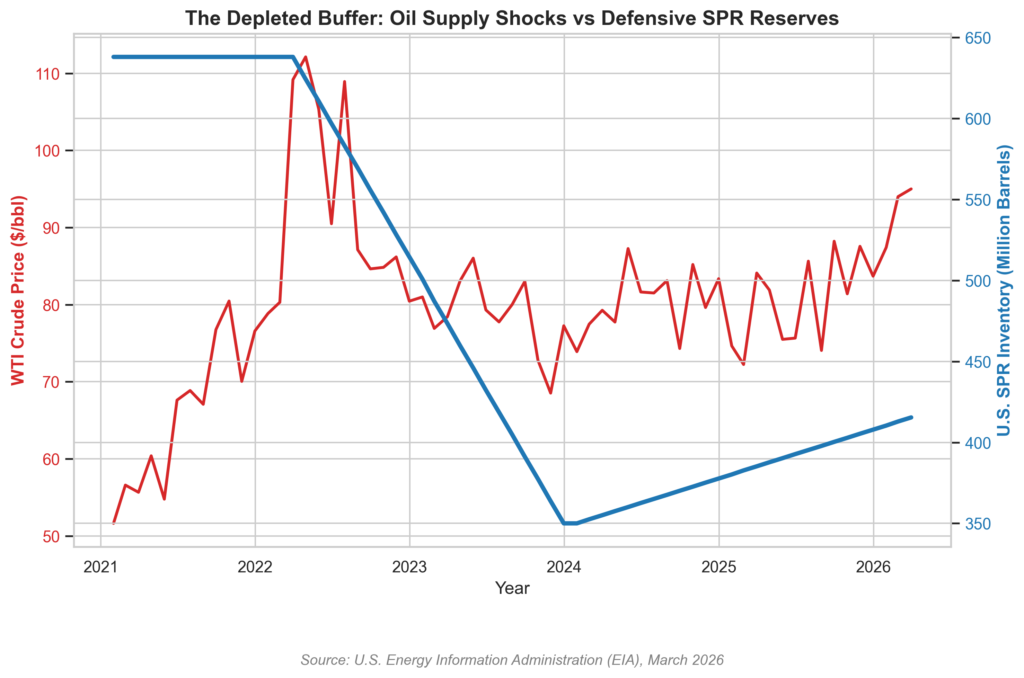

Back in early March 2026, we saw the price of WTI Crude shoot up close to $98 a barrel, and for a while during the day, it even went higher. This wasn’t just a random spike; it happened because there were real disruptions and threats to the Strait of Hormuz, which is this narrow stretch of water that handles a huge share of the world’s oil. If something actually blocks that route, there just isn’t enough spare oil production anywhere else to make up the difference, so the whole world would feel the shock almost immediately.

In the past, whenever inflation started to spike, the government responded by tapping into the Strategic Petroleum Reserve to help keep gas prices in check, which worked for a little while but used up the very resource we’d need if a real supply crisis hit. After several rounds of these emergency sales, the reserve is now much lower, and there are only so many barrels we can actually release each day because of physical and logistical limits. It’s a bit like using up your fire extinguishers when you only smell smoke, and now that there’s an actual fire in the kitchen, we’re finding the tanks are almost empty.

If you look at how the government has drawn down the oil reserves over the past few years and compare that to the price of WTI crude, you can really see how the two move in opposite directions. They used up the reserve to deal with short-term price jumps, but now we’re left with a much thinner safety net than we probably should have.

When the reserve runs low, it really changes how we have to think about riskier investments, because if something suddenly disrupts the oil supply, prices can shoot up fast and force people to use less simply because it gets too expensive. Those high oil prices feel a lot like a tax that hits everyone right away, whether you’re running a business or just filling up your car, and the effects ripple through the economy almost immediately. Suddenly, it costs more to move things around, factories have to pay more for materials, and people start cutting back on anything that’s not absolutely necessary.

If you look back, big jumps in oil prices almost always lead to a recession, because the whole economy depends on affordable energy to keep everything running smoothly, from powering factories to training those massive AI models everyone talks about. Without enough oil in reserve to cushion the blow, we lose that safety net that used to help soften the impact when things got rough.

The Federal Reserve’s mathematical trap

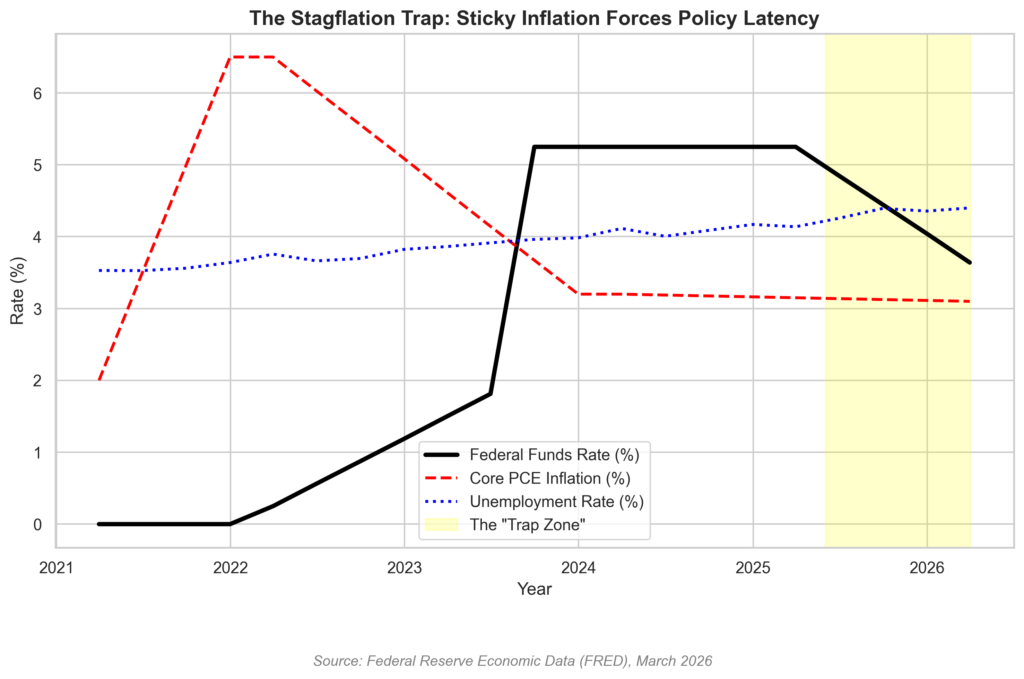

The Federal Reserve is in one of those situations where no matter what they do, there’s a real risk of making things worse somewhere else, and it’s a bit like trying to balance on a seesaw that keeps shifting under your feet. If they decide to lower interest rates or print more money to try to keep a recession at bay, there’s a good chance that prices could start rising even faster, especially since energy costs are already heading up. But if they stick with higher interest rates to keep inflation from getting out of hand, that makes life harder for companies and people who have a lot of debt, and that kind of pressure can easily show up as more layoffs.

With energy prices jumping the way they have, the Fed’s usual approach just isn’t getting the results they want. Inflation had started to calm down for a while, but now it’s picking up speed again, and by March 2026, it’s looking like any hopes of cutting interest rates will probably have to be put on hold, or maybe even dropped altogether. So, the Fed is really boxed in at the moment, without much space to try something new.

If you look at how interest rates, inflation, and unemployment are all shifting together, it feels like we’re heading into a tough stretch where the Fed has to keep rates higher than anyone really wants, just to stop inflation from running away. That kind of pressure makes things harder for businesses that need to borrow money, and we’re starting to see the effects in the job market, where unemployment is slowly rising from the low levels we’ve gotten comfortable with.

Central banks have a lot of tools at their disposal, but they can’t conjure up barrels of oil, create new shipping routes, or magically fix a broken supply chain, so when prices start rising because there just isn’t enough physical stuff to go around, rather than because there’s too much money chasing it, raising interest rates doesn’t suddenly make more oil appear; instead, it just makes life harder for everyone by squeezing demand until people can’t afford the things that are already in short supply.

All of this puts passive equity investors in a tough spot, because when growth slows down and inflation heats up at the same time, the classic 60/40 portfolio that so many people rely on can take a real beating; bonds, which are supposed to balance out the risk from stocks, end up falling too, since higher inflation pushes up bond yields and knocks down their prices just when stocks are also struggling, and the whole idea behind modern portfolio theory—that stocks and bonds usually move in opposite directions—starts to fall apart when both markets get caught in the same storm.

The deficit spiral: a $38.86 trillion structural reality

If you look at how the federal government manages its budget these days, you’ll notice that running big, ongoing deficits has become the norm, not just something we do in emergencies or during wars, but something we rely on even in times when the economy is humming along and there isn’t any obvious crisis—just to keep the basic operations going.

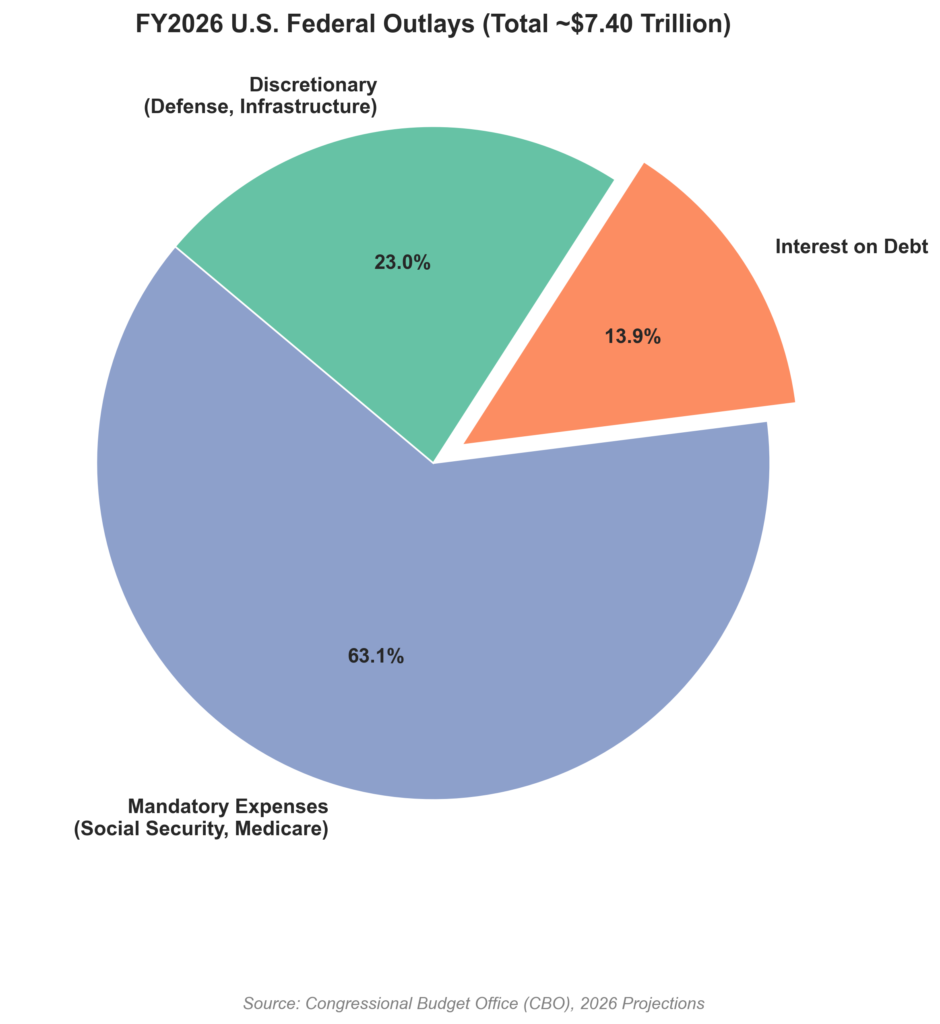

By early March 2026, the total national debt had climbed to $38.86 trillion, which means it grew by about $2.64 trillion in just one year, and while those numbers are huge and a bit hard to wrap your head around, what really starts to matter is how quickly the interest payments on all that debt are piling up.

According to the Congressional Budget Office, the government is on track to spend more than $1.03 trillion just on interest payments in 2026, which is actually starting to outpace what we spend on Medicare, and when so much of the money coming in from taxes goes straight out the door to cover interest and other required expenses, there just isn’t much left over for the government to actually make choices about where to invest or respond to new challenges.

If you try to picture how the federal budget for 2026 is divided up, it quickly becomes clear that once you set aside the money that has to go to mandatory programs and interest on the debt, there’s only a small slice left for everything else, which makes it really tough to find room for things like investing in the economy, building infrastructure, or dealing with unexpected problems.

When the government is spending a trillion dollars just on interest, it ends up in a situation where it has to borrow more money just to cover the interest payments on what it already owes, which starts to look a lot like the way a Ponzi scheme works. The tricky part is that the interest doesn’t just sit still; it keeps growing faster and faster, especially since the government has to keep refinancing its debt at whatever the current rates are, which means the average cost of borrowing keeps creeping up over time.

It’s hard to see a path where we could simply tax our way out of this deficit, since even if we took every dollar earned by every billionaire, it would only keep the government running for a short while. Cutting spending isn’t really an option either, because so many people are counting on programs like Social Security and Medicare, and it’s tough to imagine those promises being broken. So, the whole setup depends on the economy growing steadily, but that kind of growth needs both energy and money flowing through the system, and right now, both of those are in pretty short supply.

The gold revaluation escape valve

Whenever a government finds itself in a spot where the numbers just don’t add up and the debt seems impossible to manage, there are usually two main ways out: either make the currency worth less or get creative with the accounting. In the case of the U.S. Treasury, there’s actually a particular accounting move that’s completely above board and written into the rules, which involves changing how it values its official gold certificates.

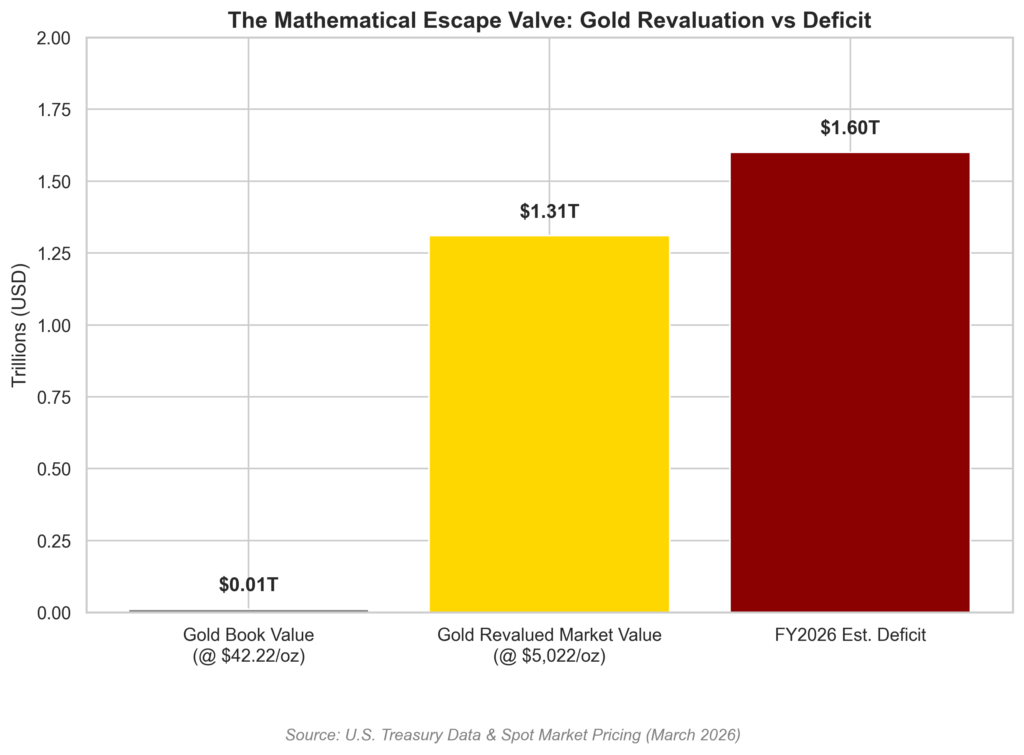

Right now, the rules say the Treasury has to value its gold at a price that was set ages ago—just $42.22 an ounce—which is wildly out of step with what gold actually sells for today. In fact, when gold prices shot up in early March 2026, hitting somewhere between $5,200 and $5,400 an ounce because of rising tensions in the Middle East and worries about stubborn inflation, it made this old book value look even more out of touch with reality.

The Treasury actually owns about 261.5 million ounces of gold, and if you use that old official price, the whole pile is only worth about $11 billion on paper, which is almost a rounding error in the grand scheme of things. But if the Treasury decided to update the value to match the current market price—let’s say around $5,300 an ounce—that same stash would suddenly be worth about $1.38 trillion, just like that.

By turning this newly recognized value into spendable money, the Treasury could put more than a trillion dollars into the financial system right away, and it could do this without needing Congress to sign off on new borrowing or asking the Federal Reserve to create new money out of thin air.

If we lay out the numbers side by side, comparing the old way the Treasury values its gold to what it would look like at today’s prices, and then stack that up next to the annual deficit, we can get a clear picture of just how much breathing room this kind of accounting move could actually give us.

What really stands out to me here is that even though $1.38 trillion sounds like an enormous amount of money—enough to make headlines and turn heads—it still falls short of covering just one year of the government’s current overspending. If the U.S. decided to revalue its gold reserves, that would be a one-off move, not something you can repeat, and it would likely send shockwaves through global currency markets because it would signal that the country is reaching for last-resort solutions to stay afloat.

If policymakers actually used this kind of escape hatch, we would probably see a big surge in the prices of things like gold and other hard assets, since people would be looking for safer places to put their money. While this might buy some time by keeping the Treasury market moving, it would also chip away at the trust people have in the U.S. dollar as the world’s go-to safe asset. And once investors start to sense that the foundation isn’t as solid as they thought, money tends to move quickly out of government debt that isn’t backed by anything tangible.

Final thoughts

When you put together $2 trillion in hard-to-see private credit, big challenges around global energy, and a deficit that has ballooned to $38.86 trillion, it becomes clear that the usual playbook for investing just doesn’t fit the current landscape. Building a portfolio that can handle all of this isn’t about hoping for the best; it’s about leaning on probability and math to guide your choices. The way bond markets have been swinging lately makes me think that the big players are already bracing themselves for some major changes ahead.

If the Treasury ever has to go through with revaluing gold, that would mark the start of a whole new era where things like gold and other tangible assets take center stage. Until that happens, though, the system will probably just keep moving along, but at a cost—higher interest rates will gradually eat into company profits and what everyday people can afford. The computers and models that run our markets are built on the idea that things will keep working as usual, but the real-world limits—both physical and mathematical—make some kind of shake-up almost certain. So the real question isn’t whether the system will have to adjust, but rather, who will end up shouldering the huge losses when the debt finally becomes too much to handle.

References

- Federal Deposit Insurance Corporation (FDIC). (2026). Quarterly Banking Profile and Default Risk Analytics.

- U.S. Department of the Treasury. (2026). Status Report of U.S. Government Gold Reserve.

- Congressional Budget Office (CBO). (2026). The Budget and Economic Outlook: 2026 to 2036.

- U.S. Energy Information Administration (EIA). (2026). Strategic Petroleum Reserve Inventory Data.

- Board of Governors of the Federal Reserve System. (2026). Federal Reserve Economic Data (FRED).

Leave a Reply