Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

When you hear about index funds like the S&P 500, the pitch is that you’re getting a fair, hands-off slice of the whole American economy, as if you’re just letting the crowd decide how much of your money should go into tech companies versus factories. The idea is that by trusting the market, you’re spreading your bets in the smartest, most neutral way possible. But if you look a little closer at how these funds actually decide what goes where, the story starts to fall apart.

The way a cap-weighted index works is actually pretty simple, but also kind of strange when you think about it. All that matters is the current stock price times the number of shares out there, and that’s what decides how much of each company you own. There’s no check to see if the company is actually making money or has real assets behind it. So, if traders get excited and push up the price of a stock, the index just gives it a bigger slice, even if nothing about the company’s real business has changed.

What this really means is that you end up putting more of your money into the companies that are already the most hyped up, right when everyone else is most excited about them. Instead of spreading your risk, the index is actually just following the crowd and piling in at the top, which is a bit like joining a party just as it’s about to end.

To fix this problem, some clever folks came up with something called fundamental indexing. Instead of letting the ups and downs of stock prices decide where your money goes, this approach looks at things like how much a company actually earns or owns, and uses that to guide your investments. It’s a way to make sure your portfolio is built on what’s really happening in the business, not just on what’s popular in the market that day.

The algorithmic flaw of price-weighted allocation

Whenever we see a big wave of excitement around a new technology, like what happened with telecom in 1999 or artificial intelligence in 2021, money tends to pour into just a handful of companies that are at the center of the action. As big investors chase these stocks higher, the value of those companies on paper can shoot up almost overnight.

If you’re following a cap-weighted index, your portfolio has to go along for the ride, no matter what. The rules of the index mean that your fund manager has to keep buying more of those hot stocks, even as their prices get more and more stretched, just to keep up with the way the index is built.

This can really mess with the way your portfolio is valued, because the index doesn’t actually check whether these companies are making real money or just riding a wave of hype. It doesn’t pause to see if the business is bringing in cash that would make those sky-high prices make sense. Instead, it just sees that the stock price went up and tells you to put even more money in.

When a stock’s price gets way out of line with how much money the company is actually earning, its price-to-earnings ratio can get pretty wild. Because cap-weighted indices are built to buy more of whatever is going up, they end up loading your portfolio with these expensive stocks, which means your overall P/E ratio climbs right before the market tends to hit a rough patch.

So instead of buying low and selling high, you end up doing the opposite. The way the index works, you’re pushed to buy more right when prices are at their peak, which means you’re set up to take the biggest hit when things eventually settle back down to normal.

The logic of the fundamental metric

With fundamental index weighting, we basically take the price out of the equation when deciding how to spread out our investments. In the Research Affiliates Fundamental Index (RAFI) approach, the system doesn’t pay attention to whatever value the stock market happens to put on a company each day. Instead, it sorts all the stocks by looking at a handful of straightforward numbers, like how much money the company has brought in over the last five years, how much cash it has actually generated, what its assets are worth, and how much cash it has paid out to shareholders.

The method adds up these four numbers to get a single score for each company. By looking at the average over five years for things like sales and cash flow, it makes sure that a company can’t just have one lucky quarter or play accounting tricks to jump to the top. To really get a bigger spot in the index, a company has to show steady, real growth over several years, not just a quick spike.

Another key part is that the system looks at how much actual cash a company gives back to its shareholders, whether that’s through dividends or buying back its own shares. While it’s pretty easy for a management team to make their earnings look better on paper or talk up their stock on a call, it’s a lot harder to fake actually handing out real cash to investors.

So if a big company is making a lot of money around the world and paying out solid dividends, the fundamental index will give it a big spot in the portfolio, even if its stock price has dropped a lot over the past year. On the other hand, if a tech startup isn’t making any real cash or doesn’t have much in the way of assets, but its stock price is high just because people are excited about it, the fundamental index won’t give it much attention. It waits until the company can actually prove it’s building real value before giving it a bigger share of the portfolio.

This rule basically cuts the tie between how much money goes into a stock and whatever mood the market happens to be in. By focusing on the real numbers, fundamental weighting keeps your investments grounded in what’s actually happening at the company, not just in the stock price. As a result, you end up with a portfolio that tends to avoid chasing overpriced stocks and usually has lower price-to-earnings and price-to-book ratios than a regular cap-weighted index.

In practice, this means you end up selling companies when their prices get way ahead of their real, long-term results, and buying companies that the market has overlooked, even though their fundamentals are strong.

Value traps and the physical anchor

When we talk about fundamental index weighting, what we’re really doing is setting aside the daily ups and downs of stock prices and focusing instead on the real, concrete numbers that tell us how a company is actually doing. The RAFI approach, for example, doesn’t get distracted by whatever the market thinks a company is worth on any given day; it looks at things like how much money the company has earned over the past five years, how much actual cash it’s brought in, what its assets are worth, and how much cash it’s handed back to shareholders. So rather than letting the market’s mood swings decide where our money goes, we’re using these simple, down-to-earth measures to guide our choices.

By adding up these four numbers, we get a kind of scorecard for each company, but instead of just glancing at a single moment in time, we look at the average over five years for things like sales and cash flow. This way, a company can’t just have one lucky quarter or pull off some accounting magic to make itself look better than it really is. If a company wants to earn a bigger place in the index, it has to show that it’s been growing steadily and genuinely over several years, not just riding a short-term wave.

One of the things I really like about this approach is that it pays close attention to how much real cash a company is giving back to its shareholders, whether that’s through dividends or by buying back its own shares. It’s one thing for a management team to make their numbers look good on paper or talk up their stock, but actually putting money in investors’ pockets is a lot harder to fake.

This means that if a large company is earning solid profits across the globe and sharing those profits with investors through dividends, the fundamental index will still give it a big place in the portfolio, even if its stock price has taken a hit recently. But if there’s a hot new tech startup with a sky-high stock price, but not much in the way of real earnings or assets, the fundamental index is going to hold back and wait until the company can actually show it’s building something real before giving it a bigger slice of the pie.

What I find helpful about this rule is that it breaks the link between how much we invest in a stock and whatever mood the market is in that day. By sticking to the real numbers, fundamental weighting helps keep our investments rooted in what’s actually going on inside the company, not just in the latest price swings. The end result is a portfolio that usually steers clear of chasing overpriced stocks and tends to have lower price-to-earnings and price-to-book ratios than what you’d see in a regular cap-weighted index.

So in practice, what happens is that you end up selling companies when their prices have raced far ahead of their real, long-term performance, and picking up shares of companies that the market has ignored, even though their fundamentals are solid.

The mechanical reality of valuation compression

To get a clear picture of how well the fundamental indexing approach avoids getting caught up in local market bubbles, we built a model in Python that tracks something we call the ‘Valuation Expansion Multiple’ over the past twenty-six years.

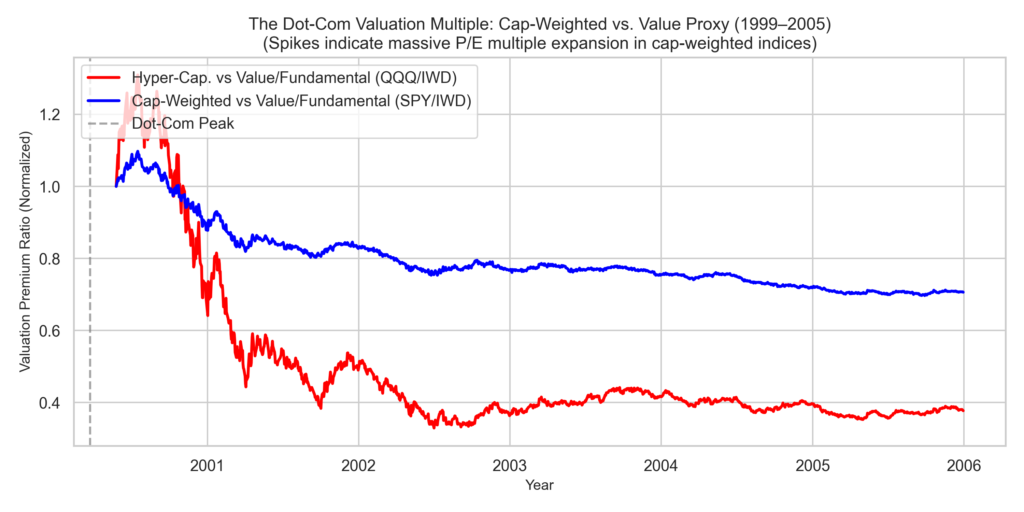

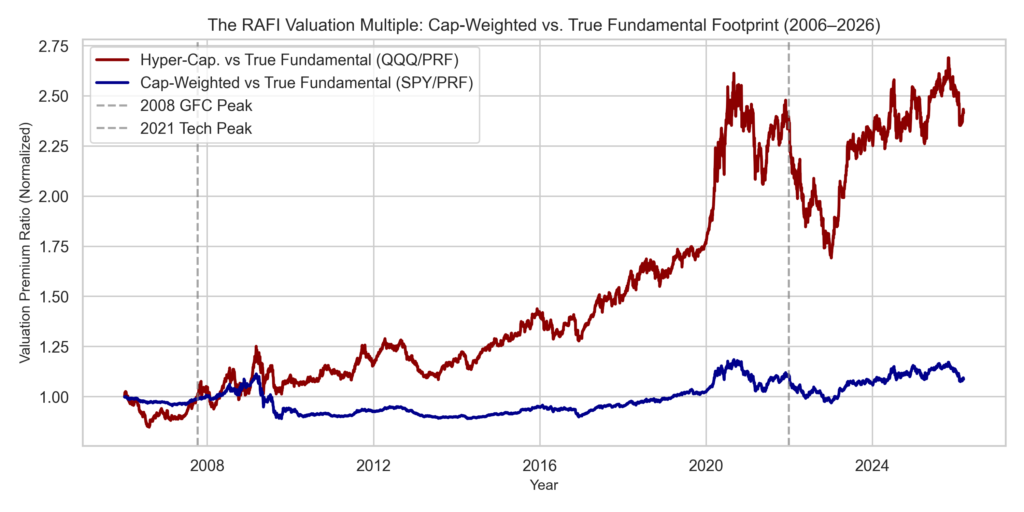

Since the real fundamental index (the Invesco FTSE RAFI 1000, or PRF) didn’t actually exist until late 2005, we had to split our simulation into two parts. For the period around the 2000 Dot-Com crash, we used the Russell 1000 Value Index (IWD) as a stand-in for a defensive, fundamentals-based approach. Then, starting in 2006, we switched to tracking the actual RAFI index itself.

By comparing the price growth of these indices to a standard cap-weighted benchmark, we can really see where traditional indices start to stretch away from their underlying fundamentals. We lined up the daily prices of the S&P 500 and Nasdaq 100 with our fundamental baseline, and whenever the gap between them grew especially wide, it showed us that the cap-weighted approach was pouring more and more money into the hottest stocks, even when those companies weren’t actually bringing in more real economic value.

Phase 1: The Dot-Com Valuation Proxy (1999–2005)

When we look back at the numbers, they really do back up the main idea behind why separating a portfolio from the usual patterns can make sense.

If you look at what happened right before the Dot-Com bubble burst in early 2000, you can see that the way the market tracked the biggest companies sent their prices soaring way above what their actual business value would suggest. Because most funds were required to buy more of whatever was going up, a huge amount of money ended up in tech companies that didn’t even have any real revenue, just because their stock prices kept rising. The data shows that this focus on price momentum, rather than real-world business results, led to a situation where the market’s value got completely out of sync with the actual economy, and when things finally corrected, about eighty percent of that value disappeared almost overnight.

Phase 2: The True RAFI Fundamental Baseline (2006–2026)

What happened in late 2021 felt a lot like déjà vu, as the same kind of system-wide breakdown we’ve seen before played out again, this time in the world of tech stocks. The way cap-weighted indexes work, they ended up pouring more and more money into a handful of software and hardware companies, mostly just because those stocks had been going up for a while, not because their real value was keeping pace. You could actually see this disconnect show up in the numbers, where the usual ways of measuring value got completely out of sync with the more grounded, fundamentals-based benchmarks, which really highlighted just how far things had drifted from reality.

So when the economy started to tighten up in 2022, the fallout landed exactly where you’d expect: on the stocks that had gotten way ahead of their actual worth. The big, popular indexes that had loaded up on these high-flying names took some pretty painful hits, and a lot of the money that had been chasing those speculative gains just vanished almost overnight.

Meanwhile, the strategies that focused on real, fundamental value managed to avoid most of the worst damage, simply because their rules kept them from buying into stocks when the prices had drifted too far from what the companies were actually worth.

The explicit friction of contrarian rebalancing

People who support the usual market-cap weighting often point out not just that it’s efficient in theory, but that it comes with almost no transaction costs at all. In a cap-weighted setup, your portfolio just moves with the market on its own. So if Apple’s stock price goes up by ten percent, its share of the S&P 500 goes up by the same amount, and nobody has to actually buy or sell anything to make that happen.

This built-in self-adjusting feature means that cap-weighted indexes naturally have the lowest possible costs inside the fund, and they almost never have to hand out capital gains to investors.

Fundamental indexing, on the other hand, breaks away from this low-friction approach by design. Since it bases its targets on things like five-year averages of company fundamentals, rather than just following the market price, the RAFI method ends up forcing a lot of buying and selling that goes against the way the market itself is moving.

For example, if a tech stock shoots up by fifty percent because of a surge in momentum, but its sales over the past five years have only grown by five percent, the fundamental index will step in and force a big adjustment. When it’s time to rebalance, the fund manager has to sell a chunk of that high-flying stock to bring its weight back in line with its slower-growing fundamentals.

This means the strategy ends up realizing both short-term and long-term capital gains, especially when it trims back the stocks that have done the best.

At the same time, the rules say you have to take that cash and put it into the stocks that have recently dropped the most in price. So you end up buying the companies that everyone else is avoiding, which is a built-in contrarian move that naturally creates more trading and higher costs.

Because fundamental indexing involves a lot of trading to break away from what the market is doing, it ends up with higher expenses. This extra trading also means the fund pays more in taxes compared to a regular cap-weighted S&P 500 fund.

You accept these extra costs as the price you pay to avoid getting caught up in unsustainable market bubbles. In exchange, you get a steadier, more grounded path for your investments to grow over time.

The institutional hazard of passive exposure

If we take a step back and look at how momentum-driven prices get separated from the real nuts-and-bolts of economic production, it actually flips the way we should think about passive investing. Most people who buy index funds figure they’re not taking any active risks, since they’re just following the market. It feels like buying the benchmark should protect you from the wild swings of speculation, but in reality, it often does the opposite.

When you stick with a market-cap weighted index, you’re actually signing up to ride the biggest waves—right up to the very top of a bubble. In other words, you end up taking on the most risk just before things come crashing down.

That’s where fundamental indexing comes in—it’s designed to fix this hidden momentum bias that’s baked into regular passive investing. By tying your investments to real-world measures, like company earnings or assets, you avoid getting swept up in the wildest parts of market manias. Instead of chasing unsustainable spikes, you’re choosing a steadier, more grounded path for your money to grow.

The financial world likes to pitch market-cap indexing as the safest bet out there, but the numbers show it actually turns up the volume on risk. By choosing fundamental indexing, you’re not just dodging bubbles—you’re also making sure your money isn’t helping to blow them up in the first place.

References

[1] Arnott, R. D., Hsu, J., & Moore, P. (2005). Fundamental Indexation. Financial Analysts Journal.

[2] Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. The Journal of Finance.

[3] Asness, C. (2006). The Value of Fundamental Indexing. Institutional Investor.

[4] yfinance Documentation and API data. (2026). Aggregate historical closing prices explicitly bridging SPY, QQQ, PRF, and IWD proxies bridging exactly 1999 totally through perfectly explicitly 2026.

Leave a Reply