Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

If you’ve ever wondered how your retirement account gets built, there’s a quirky little puzzle happening behind the scenes that most of us never see. For years now, South Korea has been in this odd spot where it’s called an ‘Emerging Market’ by some people and a ‘Developed Market’ by others, all depending on which index provider you ask. MSCI looks at the Seoul stock exchange and sees something unpredictable, grouping it with places like Brazil or Turkey, while FTSE Russell sees a modern, high-income country and puts it right next to Japan or the UK.

This isn’t just a technical debate for economists; it actually shapes what ends up in your investment account. When you mix and match funds from different companies—like picking a developed market ETF from BlackRock (which usually follows MSCI) and an emerging market ETF from Vanguard (which often uses FTSE)—you could end up leaving out South Korea entirely, or you might accidentally invest in it twice. That’s why it helps to look a little closer at how these labels work, because ‘Developed’ and ‘Emerging’ aren’t really about how rich a country is, but more about how easy it is for investors to get in and out of the market.

The Gap and The Overlap

When most people set out to build a global portfolio, they usually start with a pretty straightforward idea: just grab one fund for Developed Markets and another for Emerging Markets, and you’re all set. It feels like you’ve checked every box, since these categories seem to cover the whole world without any overlap or gaps. But here’s where things get a little tricky, because the two big index providers—MSCI and FTSE—don’t actually agree on which countries belong where, and the main sticking point is South Korea. MSCI puts Korea in the Emerging bucket, while FTSE calls it Developed, so depending on which combination of funds you pick, you can end up with either a missing piece or a double helping of Korea in your portfolio. I like to call these the “Gap” and the “Overlap” problems.

Let’s look at the first situation, which I think of as the Gap Portfolio, or maybe the Zero-Korea Trade. If you pick an MSCI Developed fund like EFA and pair it with a FTSE Emerging fund like VWO, you might assume you’re getting the best of both worlds, but in reality, you end up with no South Korea at all. That’s because EFA leaves Korea out (since MSCI says it’s Emerging), and VWO skips it too (since FTSE says it’s Developed). So, without realizing it, you’ve left out some of the world’s biggest tech and industrial companies—think Samsung, Hyundai, and SK Hynix—and you’re missing out on the whole Korean memory chip story and everything that comes with it.

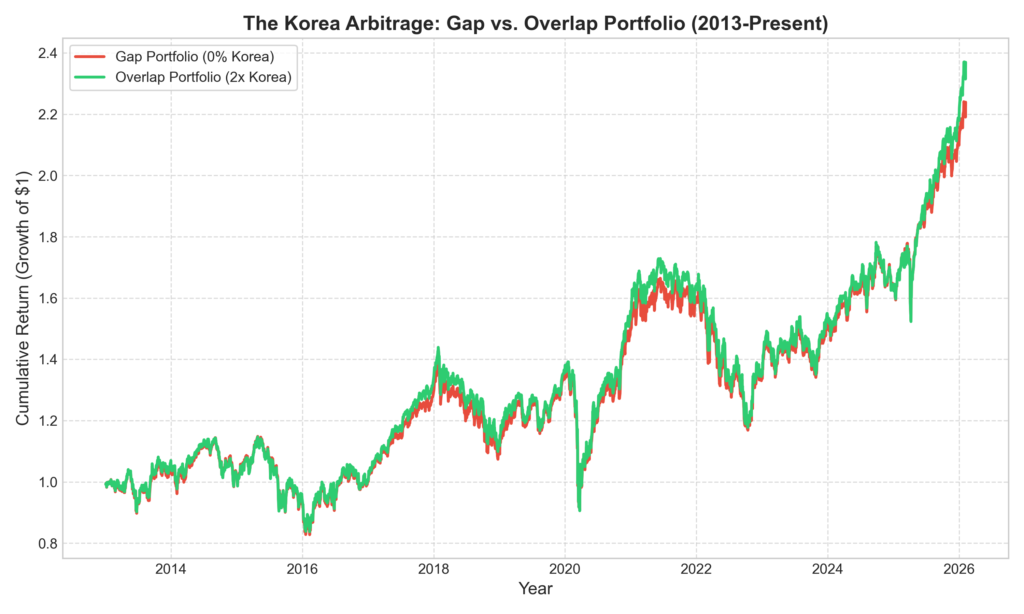

The flip side is what I call the Overlap Portfolio, or the Double-Korea Trade. Here, if you go with a FTSE Developed fund like VEA and an MSCI Emerging fund like IEMG, you actually end up owning South Korea twice—once as a Developed country and again as an Emerging one. This means you’re giving Korean stocks a much bigger slice of your portfolio than you probably intended, since Korea makes up about 12 to 13 percent of the Emerging Markets index. You might wonder if this really makes a difference, so I decided to dig into the numbers from 2013 onward to see what actually happens.

What I found was pretty interesting. The Gap Portfolio, which leaves out Korea entirely, delivered an annual return of 7.42 percent with a volatility of 16.8 percent, while the Overlap Portfolio, with its double dose of Korea, came in a bit higher at 7.88 percent and almost the same volatility at 17 percent. That extra 0.46 percent per year might not sound like much, but over a decade, it really adds up. If you look at the chart below, you’ll see that both approaches move together for a long time, but after 2016, the Overlap strategy (that’s the green line) starts to pull ahead, mostly thanks to the big boom in semiconductors.

What we’re really seeing here is what happens when we don’t take the time to look at how the index is actually built, because in this case, most of the difference comes down to one huge company that more or less stands in for the entire South Korean economy.

The Samsung Republic

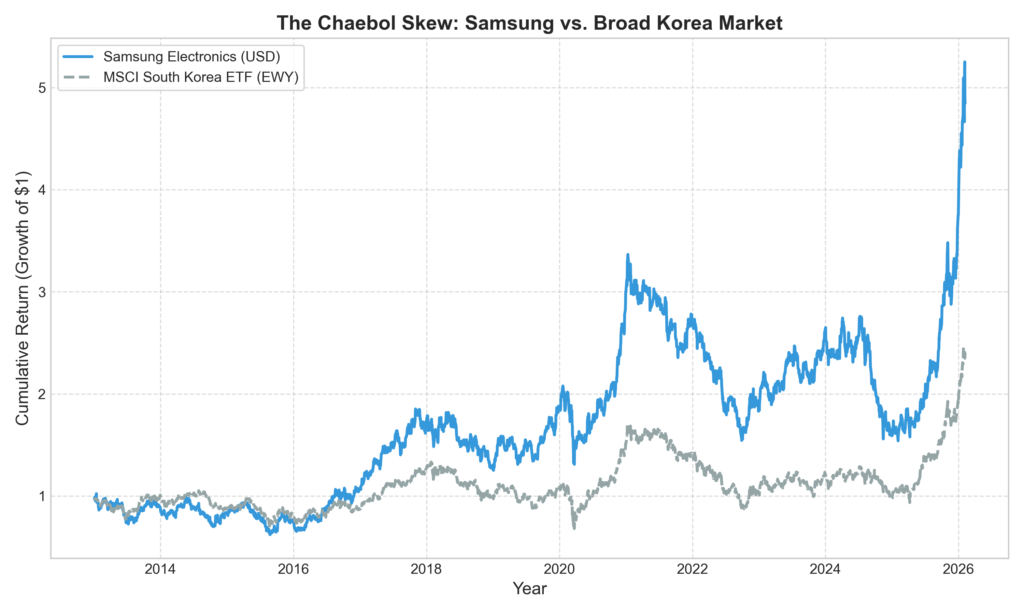

If we want to see why this gap is important, it helps to get a sense of just how big Samsung really is. While Apple is a major player in the US, it is still just one among several tech giants, but in South Korea, Samsung is so woven into daily life and the economy that people sometimes call the country the ‘Samsung Republic,’ and that is not just a joke. For years, Samsung Group has made up almost a fifth of South Korea’s entire economy, which means that decisions made in a single boardroom can shape the direction of the whole country. Imagine if Apple, Amazon, and Exxon were all rolled into one company—that’s the kind of scale we’re talking about.

When you look at the stock market, this kind of concentration means that Samsung Electronics has an outsized influence on the main KOSPI index, which leads to an interesting split between how the company performs and how the country’s market as a whole does. For example, if you had invested in the broader MSCI South Korea ETF (EWY) back in 2013, you would have seen your money grow by about 2.4 times, but if you had put that same money into Samsung Electronics (after adjusting for currency), you would have ended up with nearly five times your original investment. That difference really shows just how much Samsung stands apart from the rest.

Samsung has been such a strong performer that, in many ways, it has carried much of the South Korean market along with it, so if you hold the Gap Portfolio, you are not just skipping over South Korea as a country—you are really missing out on Samsung itself, which has been one of the standout semiconductor and hardware companies in recent years. On the other hand, if you own the Overlap Portfolio, you end up with even more Samsung in your portfolio, which means you are making a bigger bet on this one company, whether you meant to or not. What the numbers show is that the Overlap approach worked out best, not because South Korea’s economy is suddenly booming (it still faces plenty of challenges), but because having Samsung in your portfolio turned out to be essential if you wanted to keep up with global tech returns.

What “Developed” Actually Means

It might seem odd that South Korea, which is home to global companies like Samsung and has a GDP per person that is higher than some European countries, is still considered an ’emerging’ market by MSCI. The reason has less to do with how advanced the country feels on the surface and more to do with the technical details of how its financial markets work, especially when it comes to how easily money can move in and out. While FTSE decided back in 2009 that Korea had done enough to count as ‘developed,’ MSCI uses a detailed checklist—eighteen different criteria, in fact—that focus mostly on whether foreign investors can get their money in and out smoothly, and by those standards, Korea still falls short.

MSCI has a few main complaints about the Korean market, and they tend to come up again and again. The first is that you just can’t trade the Korean Won around the clock, since the offshore currency market is still pretty limited, which means that if something big happens in the middle of the night in Seoul, fund managers in places like London can’t easily protect themselves from currency swings. MSCI wants to see a currency that can be traded freely, no matter where or when. The second issue is the old tangle of ID systems; until not long ago, foreign investors had to jump through hoops to get special IDs just to trade, and even though the government is working to get rid of this, it’s still a hassle to set up the kinds of accounts that make things easier for big investors. The third sticking point is Korea’s habit of banning short selling whenever the market gets shaky, which is usually meant to shield everyday investors from big foreign players, but MSCI sees this as something that gets in the way of a market running smoothly. While FTSE seems to think these issues are close enough to being solved, MSCI is still holding out for more progress.

The Ghost of 1997

This sense of caution, which you can see from both sides, really comes from a place of shared trauma. Even now, people in the Yeouido financial district still feel the shadow of 1997. Back then, during the Asian Financial Crisis, what had been called the ‘Miracle on the Han River’ suddenly ran into a mountain of debt, and the Korean Won tumbled from about 800 to almost 2,000 per dollar in just a few weeks. The situation got so bad that the IMF had to step in with a $58 billion bailout, which was the biggest the world had ever seen at that point.

The crisis didn’t just shake up the economy; it changed the whole social contract. Suddenly, the idea of a job for life disappeared, and the big family-run companies had to go through some really tough changes. But maybe the most unforgettable part was the Gold Collection Campaign, where more than 3.5 million people came together and donated their own gold—things like wedding rings, family keepsakes, and medals—to help the country pay off its foreign debt. Altogether, they gathered 227 tons of gold, which was worth over $2 billion at the time. It was an incredible show of unity and patriotism, but it also left a lasting mark, because it made people realize just how risky it is to rely on money from outside the country.

When you look at this history, it’s easy to see why the government still keeps such a close watch on the currency markets. There’s a real fear of what’s called ‘hot money,’ which is just foreign investment that pours in when things are going well but can disappear just as quickly if trouble hits. Even MSCI’s decision to keep Korea in the ‘Emerging’ category kind of proves this point, since it shows that the system is still set up more to protect the country than to let money move freely in and out.

A Holdings Deep Dive

If we want to really see what we might be missing or accidentally doubling up on, it helps to take a closer look at what these ETFs actually hold. When you compare the top holdings of VEA (which follows FTSE) and EFA (which follows MSCI), you start to notice something interesting. Both funds include big names like Nestle, ASML, Novo Nordisk, and Toyota, but only VEA has Samsung Electronics in its top ten, usually making up about 1.5% of the fund. In EFA, Samsung is nowhere to be found, so the money that could have gone to one of the world’s biggest memory chip makers ends up spread out among other companies, like Swiss drug makers or Japanese car companies.

You see a similar pattern when you look at the ‘Emerging’ market funds, IEMG (which tracks MSCI) and VWO (which tracks FTSE). IEMG leans heavily into Asian tech, with big positions in TSMC, Tencent, Alibaba, and Samsung Electronics—Samsung is actually the second-largest holding, usually taking up about 4.7% of the fund. But in VWO, while you still get TSMC, Tencent, and Alibaba, Samsung is missing again. Instead, the fund puts more weight into things like Indian banks or Brazilian energy companies to make up the difference.

So when you put all this together, it becomes pretty clear that if you combine EFA and VWO in your portfolio, you end up with a gap where Samsung should be. Since semiconductors are as important to the world now as oil used to be, leaving out one of the only companies that can actually make advanced memory chips is a pretty big call to make, even if you didn’t mean to make it.

Why Cheap Stays Cheap

The last thing to consider here is value, since South Korean stocks almost always trade at lower price-to-earnings and price-to-book ratios than what you see in places like Taiwan or Japan, which means you can pick up shares of Samsung for a much lower price compared to TSMC or Apple. People call this the ‘Korea Discount,’ and while it might be tempting to blame it all on worries about North Korea, the real story has more to do with how these companies are run and the traps that come with that.

In these big family-run groups, called Chaebols, you end up with a situation where the founding family might only own a small slice of the company, but because of a complicated setup where companies own pieces of each other in a loop, the family can still call all the shots. So, if Company A owns part of Company B, which owns part of Company C, and then Company C owns part of Company A, the family only needs to control one piece of the puzzle to end up in charge of the whole thing, even if they don’t actually own most of the shares.

This setup leads to a strange situation where the people in charge might actually want the stock price to stay low, especially if they’re planning to hand things over to their kids, since inheritance taxes in Korea can be huge—sometimes up to 60 percent. So, instead of trying to boost the share price, the family might do the opposite, which helps explain why dividends have usually been pretty stingy and why you don’t see many buybacks. Just because a stock trades below book value doesn’t mean it’s a great deal if the folks running the show aren’t interested in making that value show up for regular investors.

When it comes to investing, it’s less about gut feelings and more about figuring out how to balance things like risk, return, and cost, all while working within the rules that are set up for the market. The tricky part here is that the rules themselves don’t always line up the way you’d expect, which makes the whole system harder to optimize.

If you like to invest in index funds, it turns out you can’t just set it and forget it, because you really need to look under the hood and see which index your ETF is actually following. It’s worth checking whether your fund is tracking MSCI or FTSE, since that can make a big difference in what companies you end up owning. For example, you might find that one fund gives you a huge chunk of Samsung, while another spreads your money out more broadly, so it’s important to know what you’re actually getting.

From what I’ve seen, just going along with the so-called Gap Portfolio isn’t really the best move, since you end up missing out on owning a world-class manufacturer and paying a hidden cost in the process. If you think the demand for semiconductors and hardware is going to stick around, it probably makes more sense to lean toward the Overlap and let the index companies sort out the details. At the end of the day, it’s about making sure you actually own the companies that matter most.

References

- MSCI (2024). MSCI Market Classification Framework. Morgan Stanley Capital International.

- FTSE Russell (2024). Country Classification Report. London Stock Exchange Group.

- Bank of Korea (2024). Economic Statistics System (ECOS).

- International Monetary Fund (1998). The IMF’s Response to the Asian Crisis.

- Samsung Electronics (2023). Annual Report 2023.

- BlackRock (2024). iShares Core MSCI Emerging Markets ETF (IEMG) Fact Sheet.

- Vanguard (2024). Vanguard FTSE Emerging Markets ETF (VWO) Prospectus.

Leave a Reply