Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

Passive index investing has always felt like a simple, almost effortless way to get the long-term growth that comes from owning a piece of the stock market, without having to constantly worry about picking the right stocks or timing the market. The whole idea works because we trust that the market, thanks to all the active traders out there, already does the hard work of sorting out which companies are worth what, so by the time our index funds buy in, most of the big mistakes have already been ironed out.

But what happens if the rules that decide which companies go into these indexes suddenly change, and now they start including huge private companies like SpaceX, OpenAI, or Anthropic, even though hardly any of their shares are actually available for regular people to buy?

The problem isn’t just that things might get a bit bumpier in the market. What really happens is that regular investors who use index funds could end up handing over money to the big players who control how these private companies go public. If we start adding companies to indexes before their prices have had a chance to settle and before there’s a real track record, it opens the door for those insiders to jump ahead and take advantage of everyone else.

When we change the basic rules about which companies get added to an index, we break the usual safety net that protects people who invest passively. Index funds could end up having no choice but to buy shares of these hyped-up private companies, no matter how expensive or unproven they are, and that acts like a hidden fee that quietly eats away at everyone’s long-term returns.

Calculating the drag of fast-track entry

When a company goes public for the first time, the people on the inside—like early investors and the banks helping with the listing—are really the ones calling the shots, since they decide exactly how much stock to put out there and when. They usually wait until their own numbers tell them the price is as high as it can reasonably get, or sometimes even higher, which means that anyone buying the stock after it starts trading is already at a bit of a disadvantage, since the odds are stacked in favor of the folks who got in early.

In the past, big market indices had a way of protecting themselves by making new stocks wait before they could join. For example, the S&P 500 asks that a company not only trades for a whole year but also shows real profits before it can be considered. This waiting period helps take the edge off the initial excitement that comes with a new listing, giving the price some time to settle down and reflect what people actually think the company is worth.

Lately, though, some other indices have started to skip this waiting period by using fast-track rules. Depending on how each index is set up, these rules can actually require that really big companies get added just a few days—sometimes as little as five or fifteen—after they first start trading.

This change makes things pretty predictable for the rest of the market, especially for the big hedge funds that use math and data to make their moves. They know exactly when these new stocks will be added to the index, so they buy up shares early, counting on the fact that index funds will have to buy in no matter what the price is. As a result, the price often shoots up right when the index funds start buying, and then, once those funds have bought at the peak, the early buyers sell their shares into that demand, which usually leads to the price dropping again.

So, in a way, regular people who invest in index funds end up paying a hidden cost, just by being the ones who always have to buy when everyone else is ready to sell.

Engineering the low-float trap

When people talk about ‘free float,’ they’re just referring to the shares of a company that regular folks like you and me can actually buy and sell on the stock market, after you take out the ones that are locked up by insiders or have other restrictions.

Apparently, SpaceX is thinking about making less than 5% of its shares available to the public when it goes public, which is a really tiny slice. In the past, having such a small amount of shares out there would have meant that SpaceX couldn’t get into any of the big stock indexes right away.

But recently, Nasdaq changed its rules. They got rid of the old requirement that at least 10% of a company’s shares had to be available to the public, and they also sped up how quickly really big companies can get added to the major indexes. A lot of people think Nasdaq did this on purpose to make sure they could attract companies just like SpaceX.

When a company goes public with only a small number of shares available, it’s a bit like trying to run a lot of internet traffic through a tiny pipe—there just isn’t enough room for everyone who wants in. Because there are so few shares and so many people eager to buy, prices can shoot up way too high at first. But history shows that once the insiders are allowed to sell their shares and a lot more stock hits the market, prices usually come crashing back down to earth, settling closer to where they probably should have been all along.

Empirical reality of the new issues puzzle

If you’ve ever felt the urge to jump into IPOs as soon as they hit the market, you’re definitely not alone, but the numbers show that this is actually one of the least effective ways to try to grow your money in today’s markets.

Back in 1995, some researchers dug into what they called the ‘new issues puzzle,’ and what they found was pretty eye-opening: people who bought IPOs just because they were new ended up with average yearly returns of about 5%, while folks who stuck with companies of similar size and risk that had already been trading for a while saw their money grow at more than double that rate, closer to 12%.

When you put together a portfolio made up only of recent IPOs, it tends to act a lot like a basket of small, unpredictable companies that aren’t making much profit, and over time, these kinds of stocks almost always fall behind the rest of the market because the real-world results just can’t keep up with all the hype that surrounded them when they first went public.

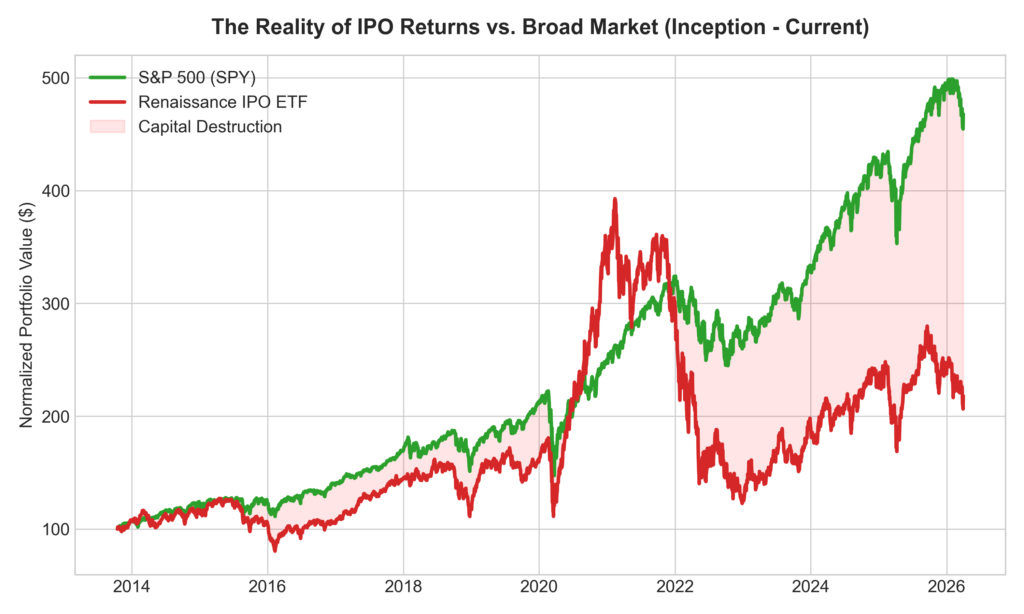

You don’t have to take my word for it, though, because we can actually see this pattern happening in real time: if you look at the Renaissance IPO ETF, which is basically a fund that just buys new public companies as soon as they’re available, and compare it to the S&P 500, you’ll notice that over the long haul—starting from when the IPO fund launched in 2013 right up to now—the IPO-focused strategy has lagged behind, no matter what market cycle we’re in.

If you look at the chart above, you can see just how rough things can get when you put too many eggs in the IPO basket. While the rest of the market kept growing steadily over the next few years, the IPO index took a huge hit, mostly because those sky-high prices came back down to earth and a wave of new shares suddenly became available for trading.

Let’s walk through a made-up example to see how this plays out with a company like SpaceX. Imagine SpaceX goes public in a hurry and ends up with a $1.75 trillion price tag, but only puts 5% of its shares out there for people to buy. That would mean its price-to-sales ratio would shoot up past 100, which is wild when you remember that the average for the whole S&P 500 is only about 3.1. When you mix super high starting prices with not much stock available, it usually means future returns are likely to be a lot lower.

The thing is, private companies tend to go public right when they think they can get the highest possible price, so if you’re buying in just because an index tells you to, it’s a bit like showing up to a party exactly when the snacks are running out and the prices are highest—it’s just not a great deal.

Researchers have found that this kind of buying—where you’re almost forced to jump in at the worst possible moment—can quietly chip away at your returns year after year, costing index fund investors somewhere between half a percent and three-quarters of a percent annually, just because of how these big changes get added to the index.

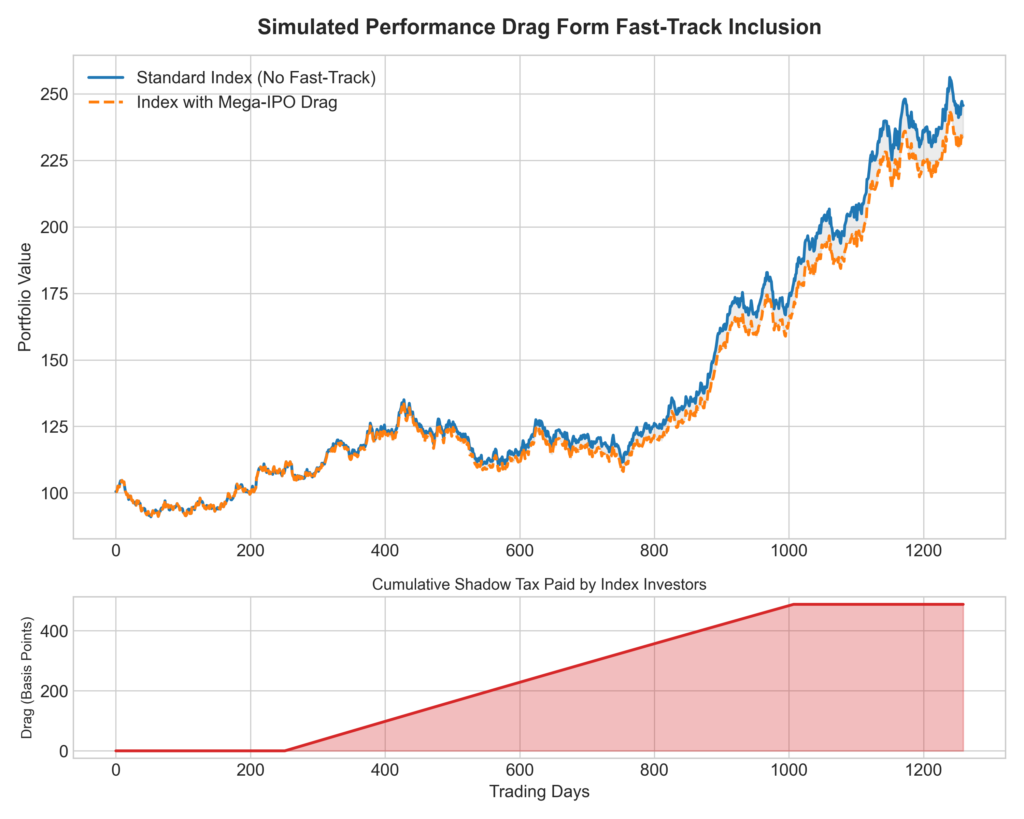

To make this easier to picture, I ran a simple simulation comparing a regular market index to one that suddenly adds a giant IPO with a big 10% slice, only to see that new addition drop by half in value soon after.

What you see in the bottom panel is really just a way of showing how much of the passive investor’s expected return quietly gets chipped away over time. When that money gets pulled out and handed over to the active traders—because the rules force the passive funds to buy certain stocks—the loss doesn’t just happen once. Instead, it keeps building up, making it harder for the portfolio to catch up.

That’s actually the main reason why a lot of big, experienced investors go out of their way to use strategies that help them dodge this problem. For example, some funds—like those run by Dimensional Fund Advisors—try to match the market as a whole, but they make a point of waiting a full year before buying any brand-new IPOs. By doing this, they avoid getting caught up in the rush for these new stocks, which often turn out to be overpriced and risky, so their portfolios end up steering clear of the worst trouble spots.

Capital destruction in the pre-IPO illusion

Sometimes, investors get so excited about a company that they try to get in early by looking for ways to buy shares before the company even thinks about going public.

But for regular folks who want a piece of these private companies before everyone else, the path is usually full of big fees, confusing legal hoops, and sometimes even scams that are hard to spot until it’s too late.

For example, there was a real investment fund set up just to let regular investors buy private shares, but it charged a huge 4% fee right at the start and then took a quarter of any profits you might make later. By the time all the middlemen take their cut, there’s not much left for you, even if the company’s value goes up.

Even experienced investors who try to get in through fancy new funds that promise access to private companies have sometimes lost money, even when the companies themselves look like they’re worth more on paper. It turns out that if you’re buying into the most talked-about private deals, you might just be paying top dollar to the people who got there first.

Right now, it feels like the rules of the public markets are being changed so that regular investors end up providing a big exit ramp for the huge private equity funds. It makes me wonder what will happen to things like index funds and how well markets work if, for the next decade, everyone has to play by these new, fast-tracked rules.

References

- Loughran, T., & Ritter, J. R. (1995). The New Issues Puzzle. The Journal of Finance, 50(1), 23-51.

- Historical S&P 500 Price-to-Sales Market Data (2026).

- Nasdaq-100 Fast-Track Methodology Changes (2026).

- SEC filings and fee structures analysis for selected Pre-IPO Special Purpose Vehicles.

Leave a Reply