Disclaimer: The opinions expressed in this article are my own and do not represent the views of Google. This content is based solely on publicly available information.This content is for educational and entertainment purposes only. The author is not a financial advisor, and the content within does not constitute financial advice. All investment strategies and financial decisions involve risk. Readers should conduct their own research or consult a certified financial professional before making any financial decisions.

If you look at what’s happened since 2010, you’ll see that about eighty percent of the money going into the US stock market has ended up in passive funds run by just three big companies. A lot of people think this is a safe and sensible way to invest, because it feels like you’re just buying a little piece of everything and letting the market do its thing. The idea is that by owning a broad index fund, you’re simply reflecting the real economy, with all its different industries and companies. But here’s the twist: when so much money moves this way, it actually starts to change how the market works at a basic level, in ways most people don’t expect.

When all this money pours into index funds run by Vanguard, BlackRock, and State Street, it doesn’t really stop to ask whether a company is actually a good business or if its stock price makes sense. Instead, the money just follows a simple rule: buy more of the companies that are already the biggest. So, rather than looking at things like how much cash a company brings in or how much debt it has, the system just keeps feeding the giants, which means that being big today almost guarantees you’ll get even bigger tomorrow.

Mechanics of passive liquidity flows

If you look at how index funds work, especially those that track the S&P 500, you’ll notice that the way they spread your money around is a bit like a momentum machine running on autopilot, even though it’s packaged as a safe retirement plan. When you put a dollar into one of these funds, only a tiny sliver of it actually goes to the smallest companies in the index, while the biggest players at the top get the lion’s share. The thing is, the fund doesn’t stop to ask whether those big companies are healthy or fairly priced; it just keeps buying more of whatever has already gone up.

This setup ends up bending the way prices work across the whole stock market, because unlike an active fund manager—who tries to figure out if a stock’s price actually makes sense based on what the company might earn in the future, and who will usually stop buying if things get too expensive—index funds just keep buying, no matter what. There’s no built-in check to stop them from pouring more money into stocks that might already be overpriced.

Since so many people are automatically enrolled in retirement plans that buy these broad market funds every couple of weeks, there’s a steady stream of money flowing into the stock market, regardless of whether prices are high or low. The rules of the index mean that the bigger a company gets, the more of this automatic money it attracts, so the largest stocks keep getting a bigger slice of each new round of investment.

What ends up happening, thanks to the math behind all this, is that a small group of really big companies soak up most of the benefit from this constant flow of money. Because the buying doesn’t care about price, their stock prices get pushed up even more, which makes them an even bigger part of the index, so the next round of automatic investments buys even more of their shares. It’s like a feedback loop that keeps feeding on itself, with prices rising just because they’ve already gone up, not because anything real has changed about the companies themselves.

The illusion of corporate performance

If you read the news, you’ll notice that people often talk about how the biggest tech companies make so much money, and that’s usually given as the main reason for why they’re on top. It’s true that these companies bring in a ton of cash, but that’s only part of the story. The rest of their huge stock price gains actually comes from something a bit less obvious: the market just keeps deciding to pay more and more for each dollar these companies earn, which is what people call multiple expansion.

You can actually see this play out if you look at the numbers for the biggest companies in the stock market over the past sixteen years. From 2010 to early 2026, the total value of the top five companies went up by about ten times, which is pretty wild. Even though these tech giants did grow their profits a lot during that time, their stock prices shot up way faster than their actual earnings did.

If you dig into the old market data, you’ll see that back in 2010, one of the top five biggest stocks usually traded at about sixteen times its earnings, which was pretty normal for the market. Fast forward to 2026, and that number jumps to over thirty-four times earnings for those same top spots. In other words, investors are now happy to pay more than twice as much for each dollar these companies make, compared to what they used to.

This jump in how much people are willing to pay isn’t really because the businesses themselves are suddenly growing faster. Instead, it mostly comes down to how money flows into the market these days. When lots of investors put their cash into index funds to spread out their risk, they end up buying more and more of the same handful of giant tech companies, whether they mean to or not.

Multiple expansion in mega-caps quantified

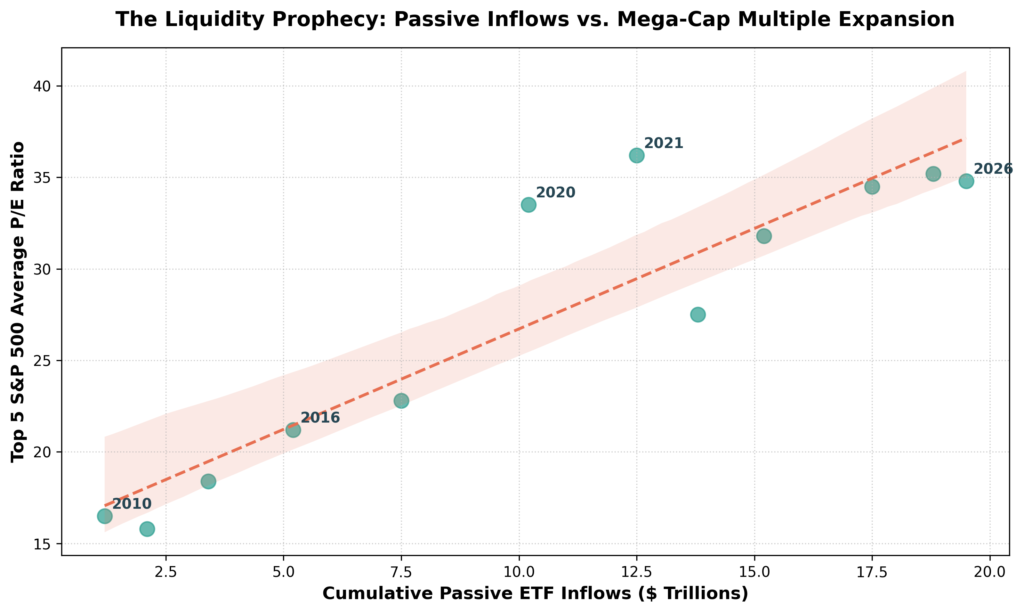

To really see how these two things move together, I lined up the total amount of money flowing into passive ETFs around the world (measured in trillions of dollars) right next to the average price-to-earnings ratio of the five biggest companies in the S&P 500 from 2010 to 2026. When you look at the numbers side by side, the connection jumps out in a way that is both clear and a little unsettling.

When I ran the numbers on all this data, I found that the link between the flood of passive money coming into the market and the rising price-to-earnings ratios of the biggest stocks is incredibly strong—about 0.91, if you like statistics. What this means in plain terms is that for every extra $1 trillion that flows into passive funds, the average P/E ratio of the top five companies goes up by about 1.1 points. It is almost like there is a hidden rule quietly shaping the market behind the scenes.

What is wild is that this growth happens no matter what is going on with company earnings, new products, or even big changes in interest rates. It really just comes down to the way money moves. If you look at the chart below, you can see how this steady stream of passive buying keeps pushing up the value of the biggest companies, almost like an invisible force quietly inflating their prices year after year.

The concentration paradox

I think it’s worth looking at the mindset behind this whole situation, because a lot of regular investors keep putting their money into the S&P 500, mostly because they trust it will shield them from the risk of any one company blowing up. The idea is that by buying the index, you’re spreading your bets and avoiding putting too many eggs in one basket. But here’s the twist: since these index funds decide what to buy based on which companies are already big and have been doing well, what you actually end up with today is a portfolio that’s more concentrated in a handful of giant companies than ever before.

It’s kind of a funny contradiction, isn’t it? The tool that’s supposed to give you the most diversification actually ends up making you bet really heavily on just a few big tech companies, as if they’ll always keep their sky-high prices.

Normally, the thinking goes that as a company gets bigger, it should start to slow down just because there’s only so much market left for it to grab. But with passive indexing, that slowdown doesn’t really happen the way you’d expect, since the index keeps pouring money into the biggest winners without asking whether they’re still growing or not. This ends up making it much cheaper for these giant companies to raise money, which gives them a huge edge over the smaller, possibly more creative businesses that don’t get nearly as much attention.

The algorithmic fragility of modern markets

When we really look at the numbers, it gets a bit uncomfortable, because it turns out that the S&P 500’s steady, low-drama outperformance over the last decade has a lot to do with the way passive investing keeps growing, rather than just the strength of the companies inside the index.

A big reason the index keeps doing so well is that people and institutions all over the world keep buying it, no matter what the price is, instead of just because the companies themselves are suddenly twice as productive. So, a lot of the recent gains might be more about the steady flow of money coming in than about real, lasting improvements in the businesses themselves.

The biggest companies at the top of the index are caught in a kind of feedback loop, where their huge size keeps attracting more money just because they’re already big. This cycle can keep going for a long time, as long as more new money keeps flowing in from passive investors than is leaving the market from people cashing out for retirement or big funds rebalancing their portfolios.

Sooner or later, every imbalance in the financial world has to face the music. If the market depends on a steady stream of automatic money just to keep prices high, it could be in for a rough time if that flow ever slows down. Index funds are great at keeping costs low over the long haul, but anyone leaning hard on this passive approach should really stop and think: what happens to those high prices if the easy money stops coming in, and the companies have to actually earn enough to justify those big valuations?

References

[1] Global ETF Market Growth and Capital Flows 2010-2026, Companies Market Cap Data.

[2] Passive Investing and Market Concentration, FactSet Earnings Insight historical reports.

[3] Valuations and Multiple Expansion in Mega-Cap Technology, YCharts historical market reports.

Leave a Reply